Economic uncertainty prevails on the back of general weakness

The broad economic themes that kicked off 2024 remain in place, with economic weakness, unemployment moving higher and inflation set to fall to the RBA’s 2 to 3 per cent target.

The broad economic themes that kicked off 2024 remain in place, with economic weakness, unemployment moving higher and inflation set to fall to the RBA’s 2 to 3 per cent target.

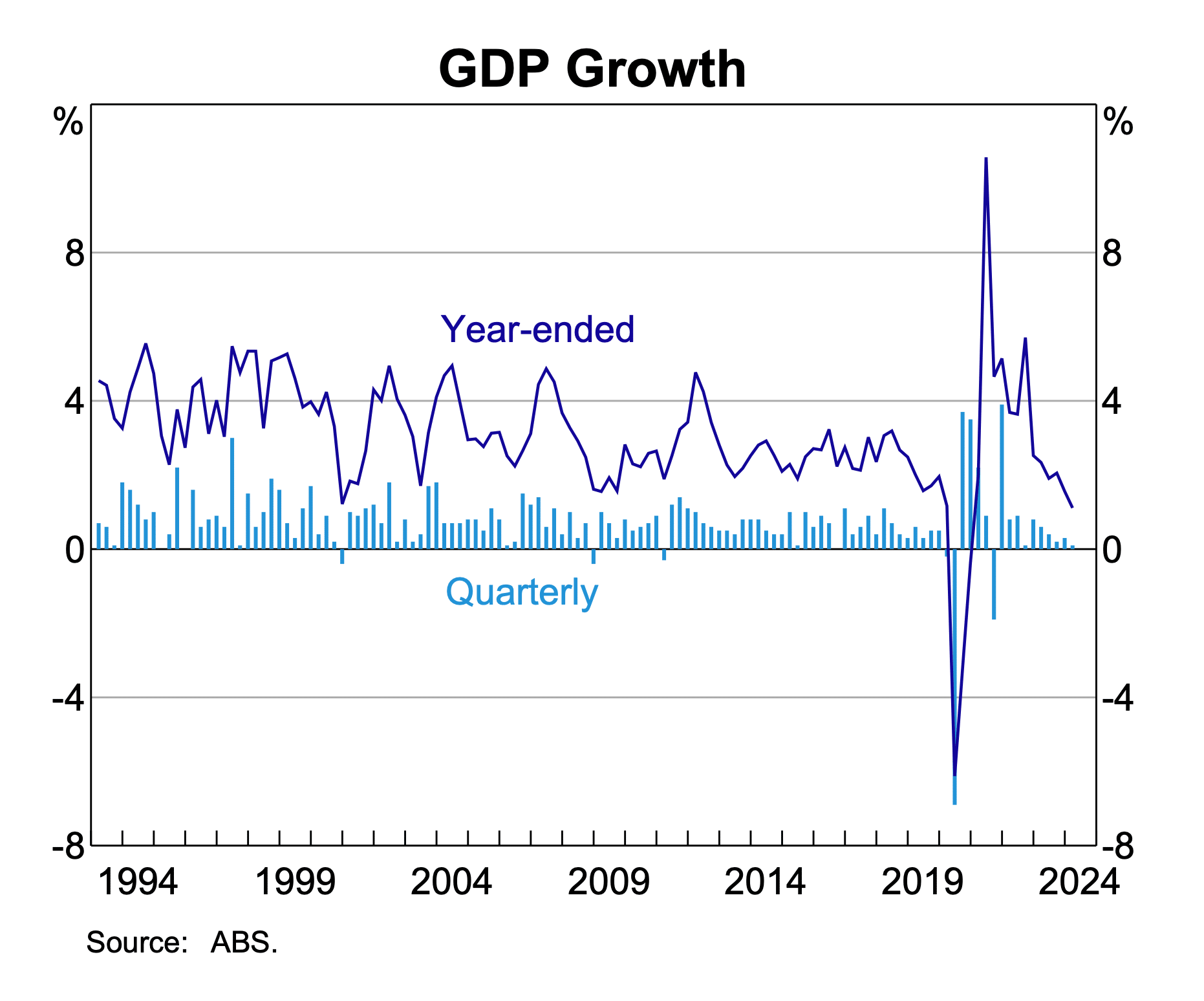

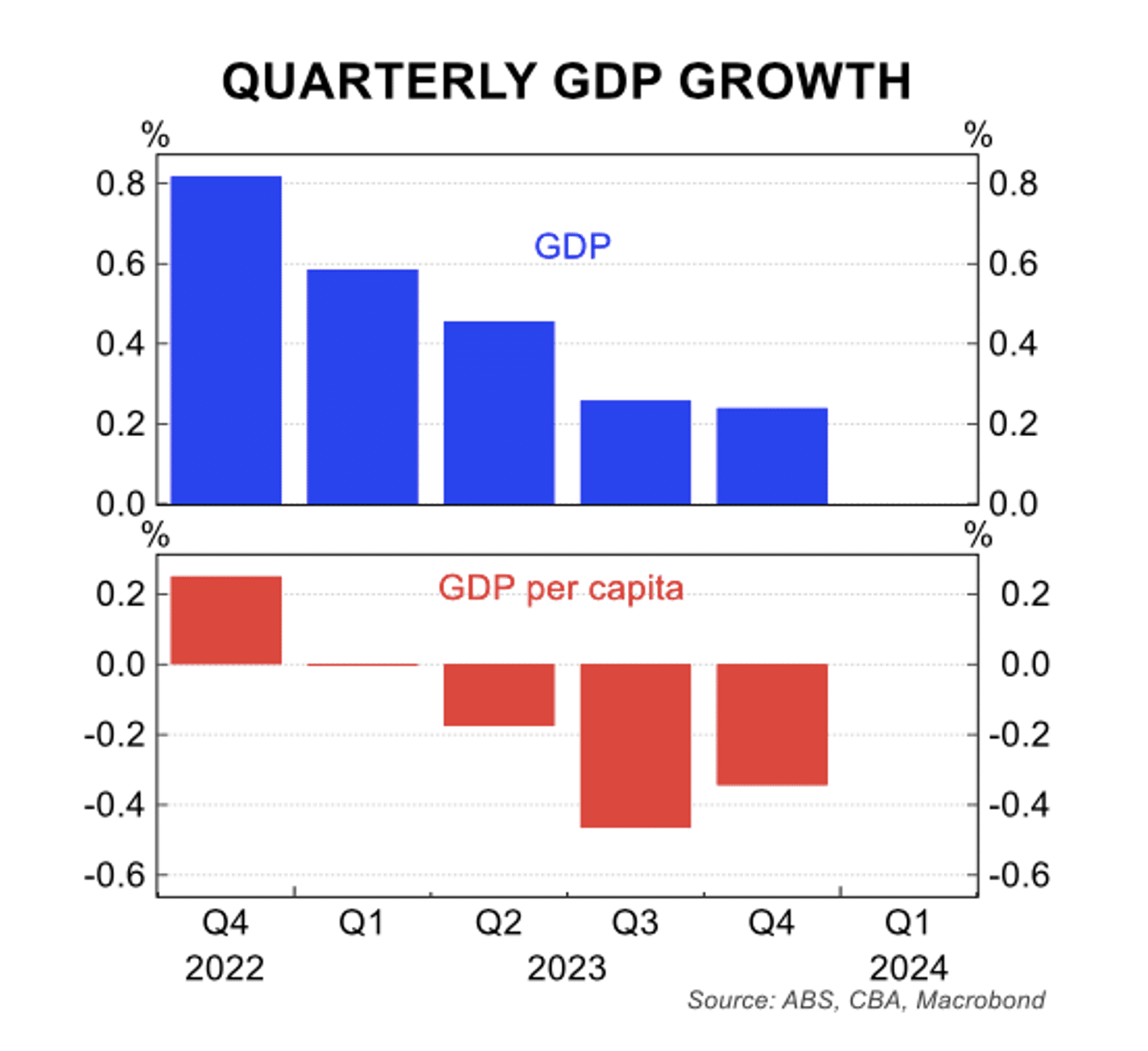

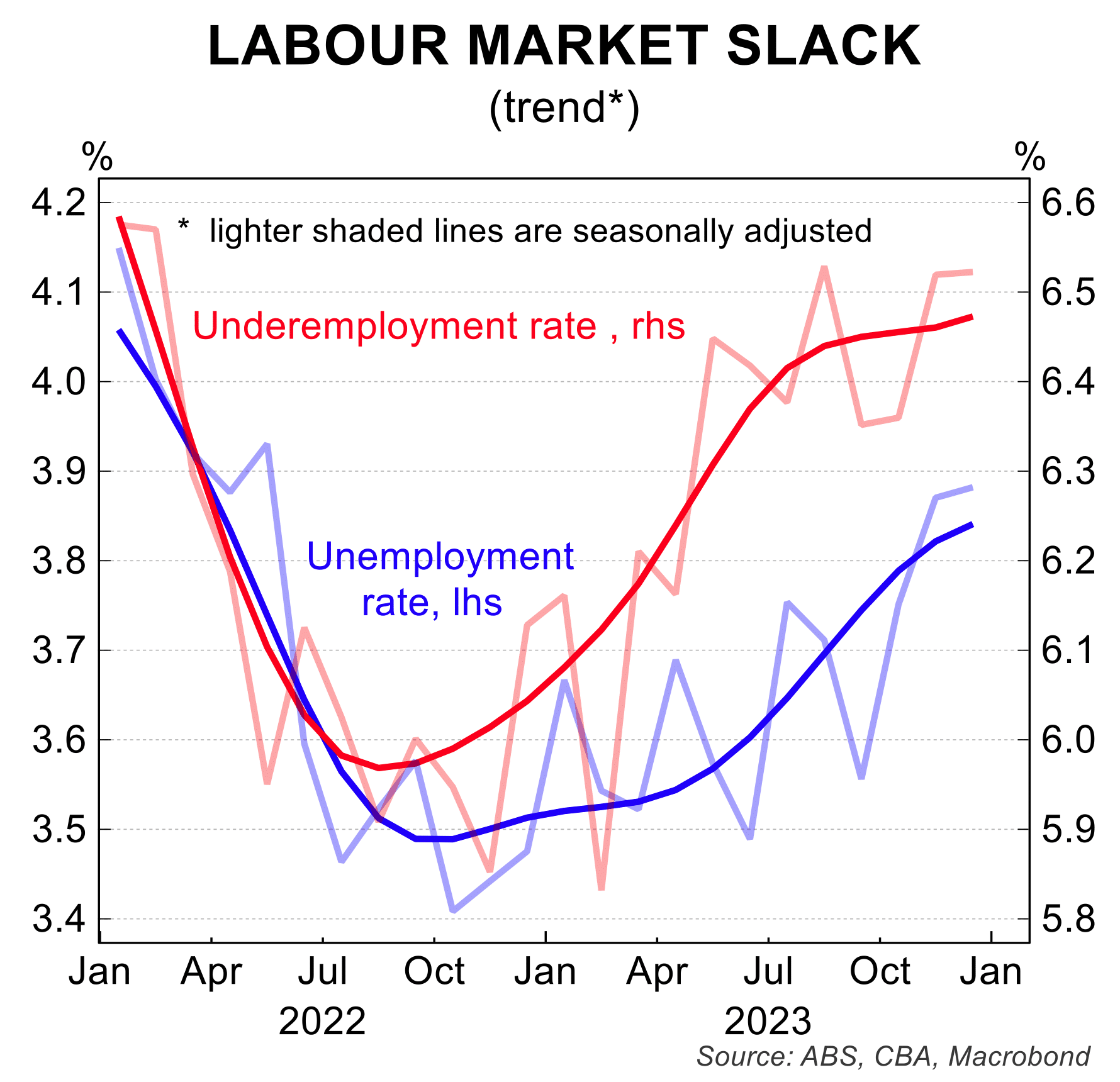

The past month was dominated by news of weaker economic growth, a still fragile labour market and an upward blip in inflation. There was no surprise when RBA left interest rates steady at 4.35 per cent after its June meeting, meaning there has been no policy change since the last rate hike in November 2023.

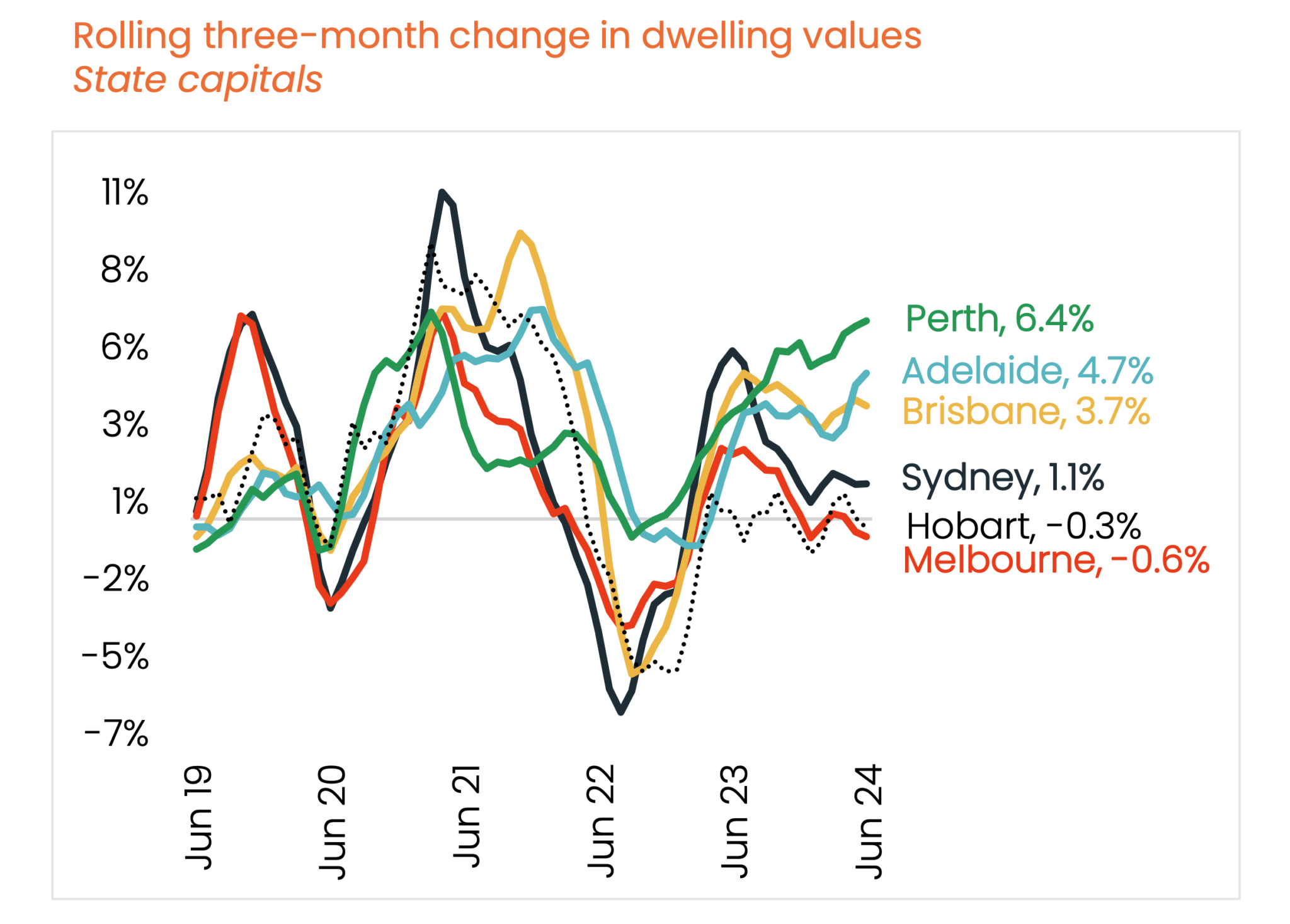

The Australian property market continues to deliver stable results in most jurisdictions despite the higher cost of living currently being experienced by many Australians… The construction sector remains tight with pressure on supply-chains relating to materials and labour evident, however we are seeing trends suggesting we are at, or very close to, the top of the price-hiking cycle.

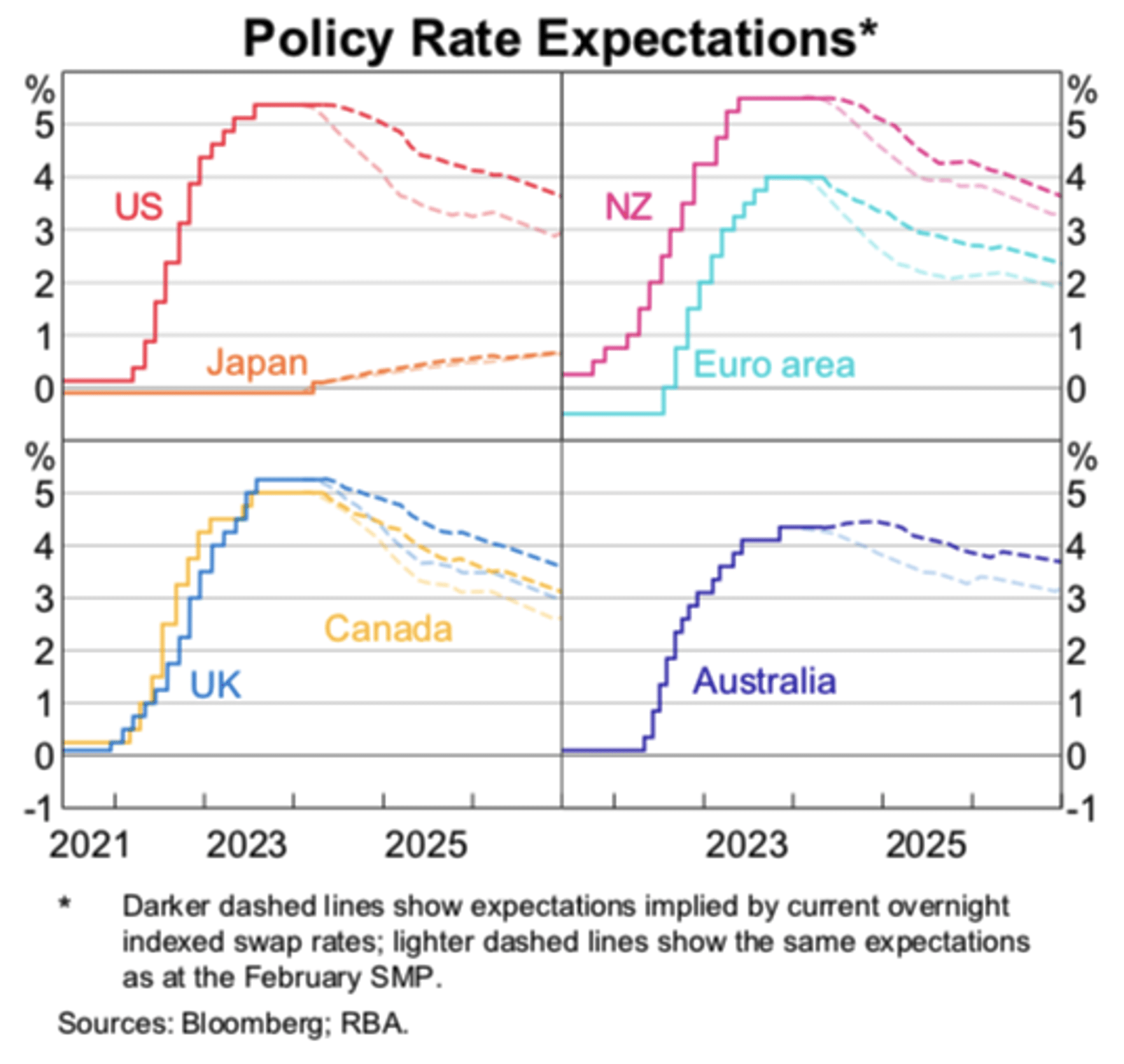

Markets are volatile. Weak economic conditions and falling inflation has rekindled expectations of interest rates cuts in Australia and much of the industrialised world in coming months… The next readings on inflation and unemployment will be critical in the timing of those cuts.

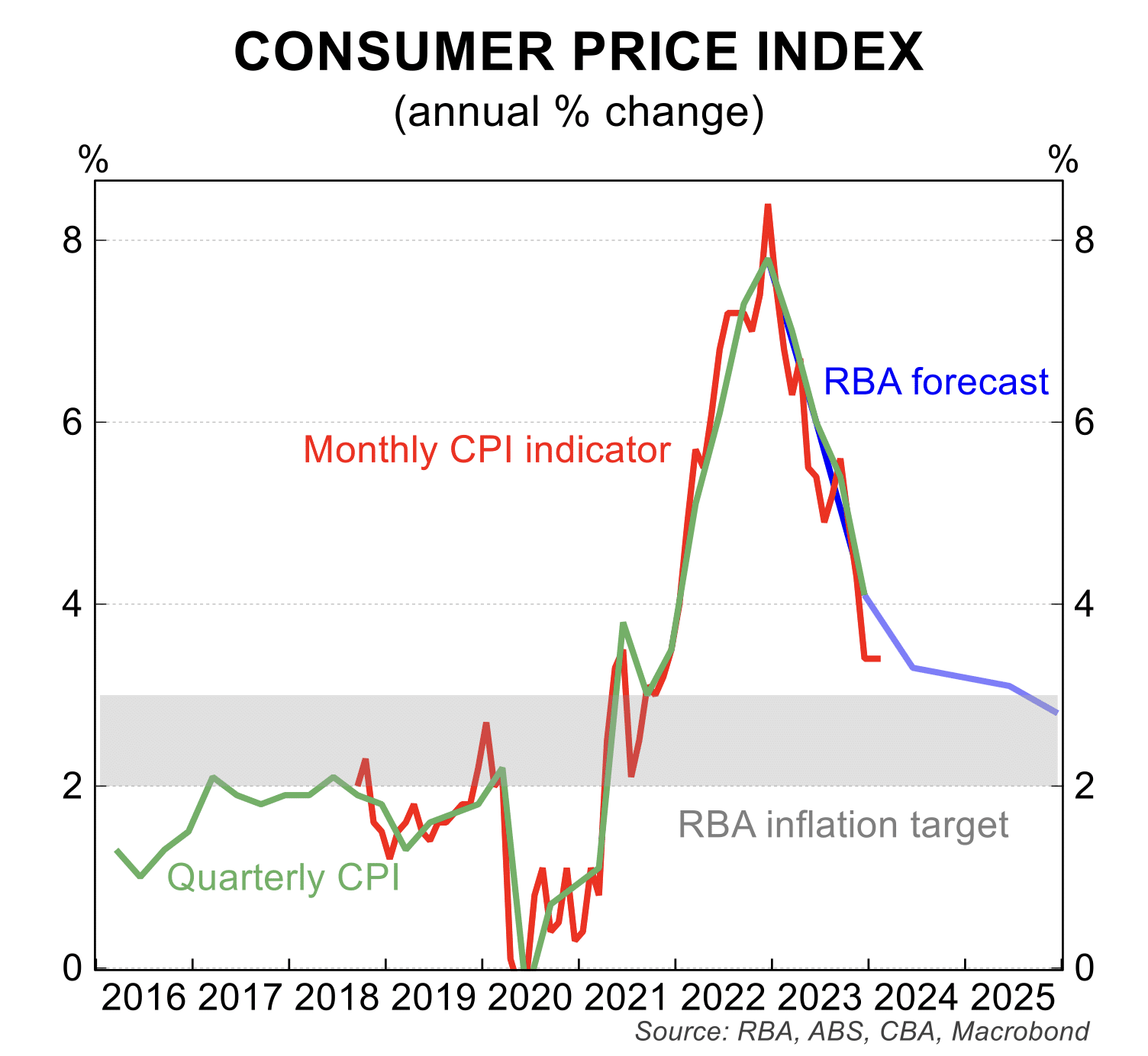

The Australian economy has continued to track at a low growth rate with inflation continuing to ease. As a result of these trends, the RBA has moved to a clear neutral bias dropping the ‘next move is likely to be up’ comments at its March meeting.

NSW continues to grapple with a significant housing shortage. Economic forecasts project a substantial increase in population over the next five years, further exacerbating the current housing situation… Looking forward, we remain buoyed by the market opportunity for us to fund many future projects.

While there remain reason to be cautiously optimistic about the outlook for the economy later in 2024, the RBA needs confirmation that inflation is tracking towards the mid-point of its 2 to 3 per cent before moving to cut rates. This is likely to come the next quarter or two as the current sluggish growth dampens the pricing power of business and with that inflation is driven lower.

There are reasons to expect a better second half of 2024 for the economy: Income tax cuts will take effect from 1 July 2024, the prospect for interest rate cuts, rising real wages and a positive wealth effect for households from housing and the strength in the stock market.

As we approach the end of the interest rate rising cycle, we are seeing various indicators stabilise, including building materials, supplies, and stock. This is a positive sign that the market is adjusting, and we are closely monitoring these trends.

Cost pressures, labour costs and the interest rate hiking cycle have been headwinds to the sector in 2023. For 2024, with cost pressures easing and the labour market problems abating, the sector is poised for a stronger 2024 and 2025.

The broad economic themes that kicked off 2024 remain in place, with economic weakness, unemployment moving higher and inflation set to fall to the RBA’s

The past month was dominated by news of weaker economic growth, a still fragile labour market and an upward blip in inflation. There was no

The Australian property market continues to deliver stable results in most jurisdictions despite the higher cost of living currently being experienced by many Australians… The

Markets are volatile. Weak economic conditions and falling inflation has rekindled expectations of interest rates cuts in Australia and much of the industrialised world in

The Australian economy has continued to track at a low growth rate with inflation continuing to ease. As a result of these trends, the RBA

NSW continues to grapple with a significant housing shortage. Economic forecasts project a substantial increase in population over the next five years, further exacerbating the

While there remain reason to be cautiously optimistic about the outlook for the economy later in 2024, the RBA needs confirmation that inflation is tracking

There are reasons to expect a better second half of 2024 for the economy: Income tax cuts will take effect from 1 July 2024, the

As we approach the end of the interest rate rising cycle, we are seeing various indicators stabilise, including building materials, supplies, and stock. This is

Cost pressures, labour costs and the interest rate hiking cycle have been headwinds to the sector in 2023. For 2024, with cost pressures easing and