Our strategy remains firmly focused on disciplined, conservative growth. Safeguarding our investors’ capital is our highest priority. For FY26, our objective is to continue increasing FUM by sourcing high-quality opportunities

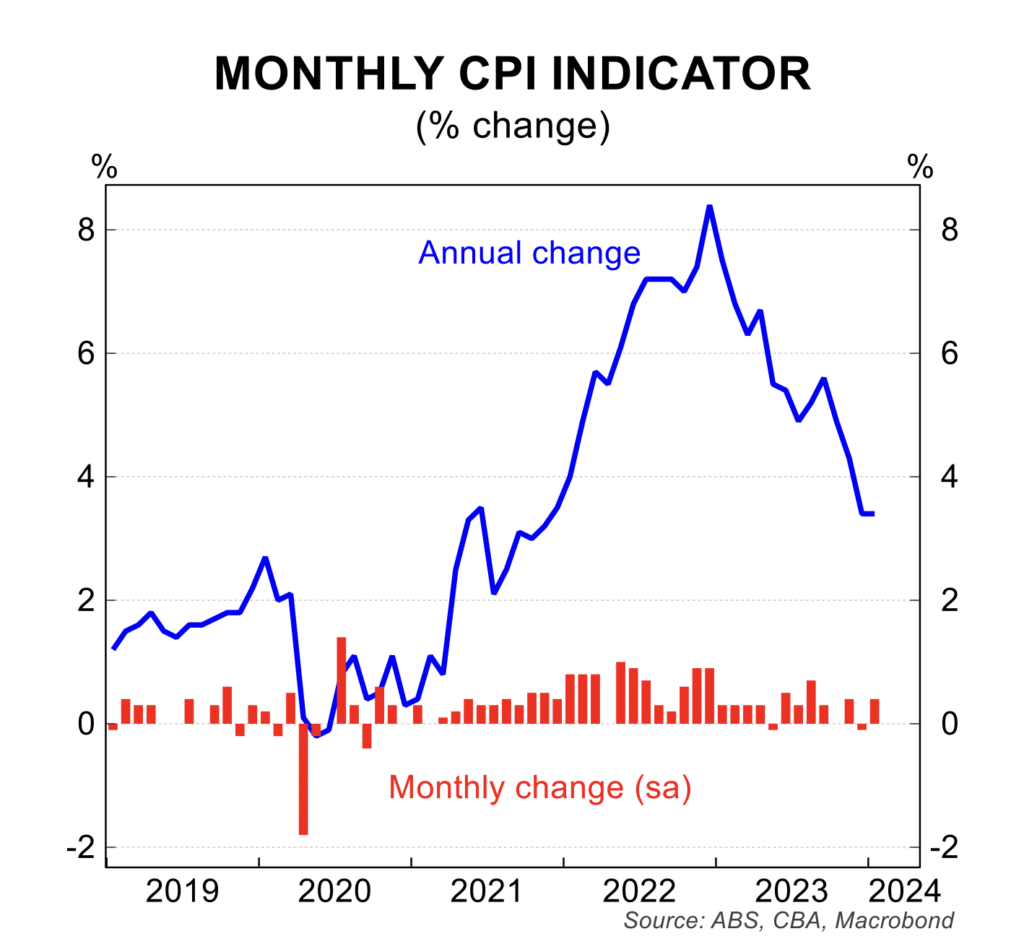

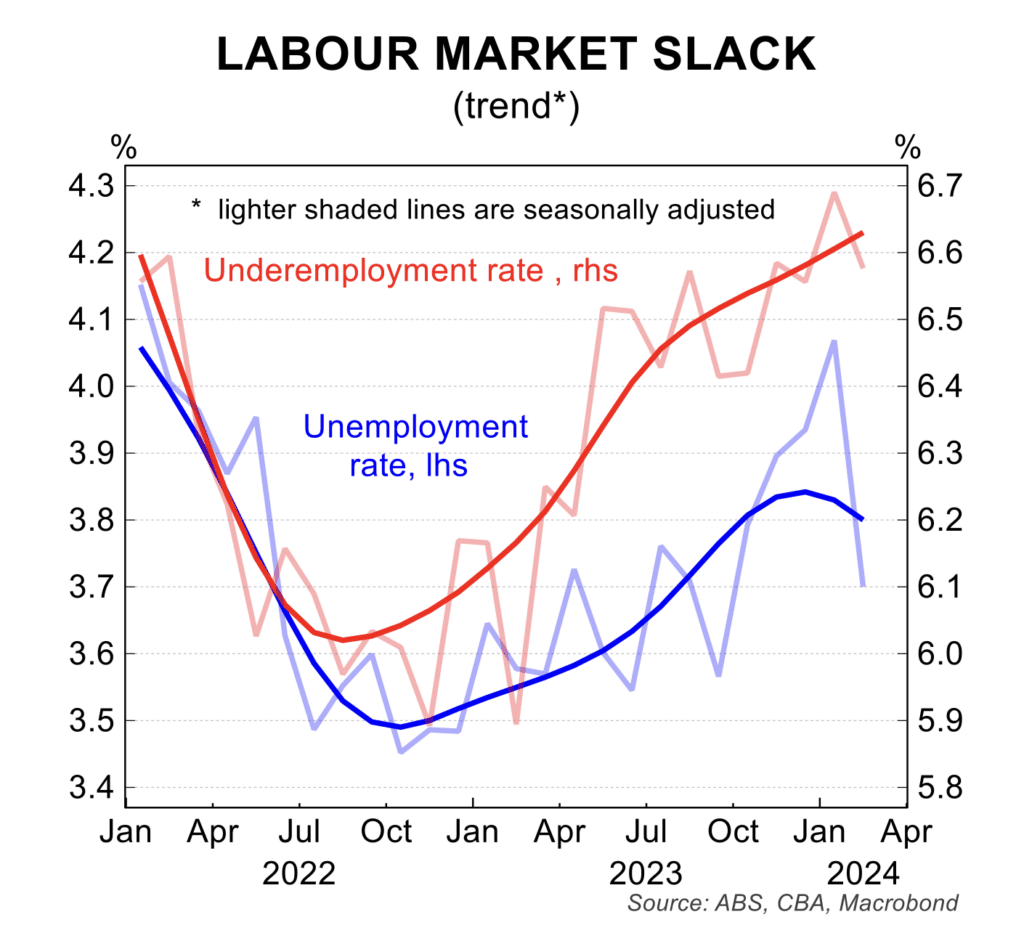

The Reserve Bank of Australia surprised markets and economists alike this month by holding interest rates steady, despite clear signs that inflation is returning to target levels. The decision, announced

In this update, we share an overview of the current market environment and highlight how we are adapting to changing conditions while remaining focused conservative and prudent risk management.