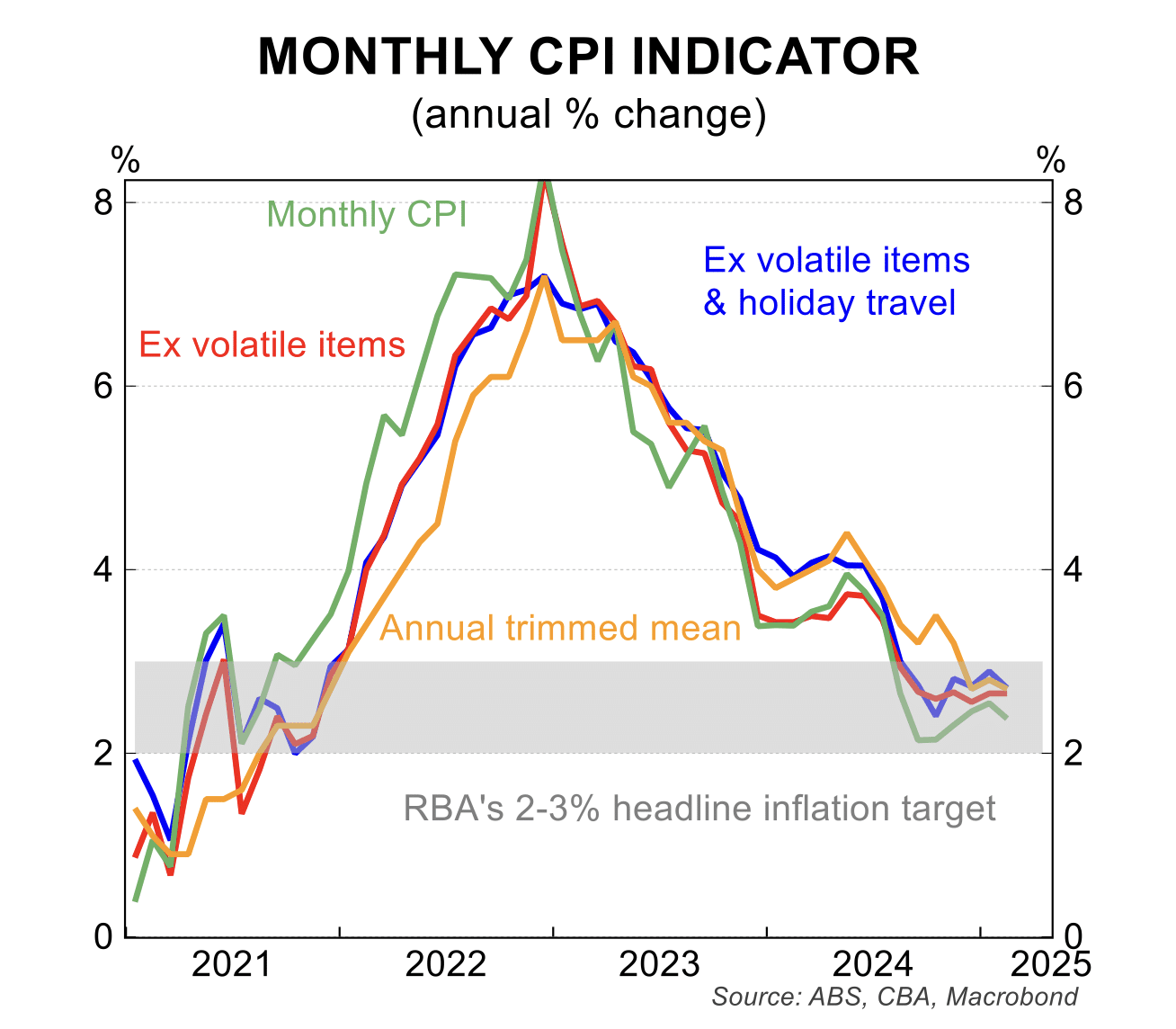

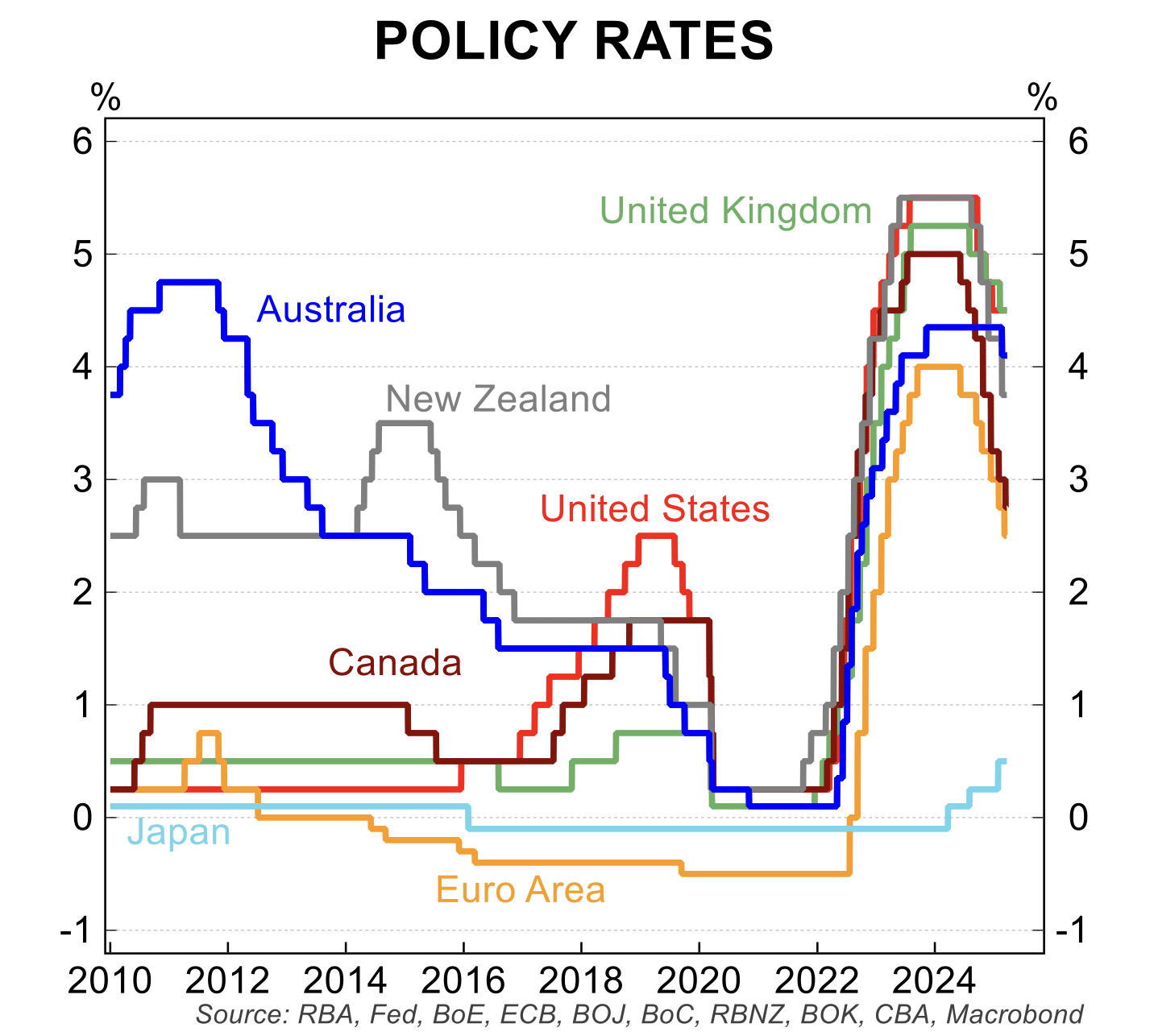

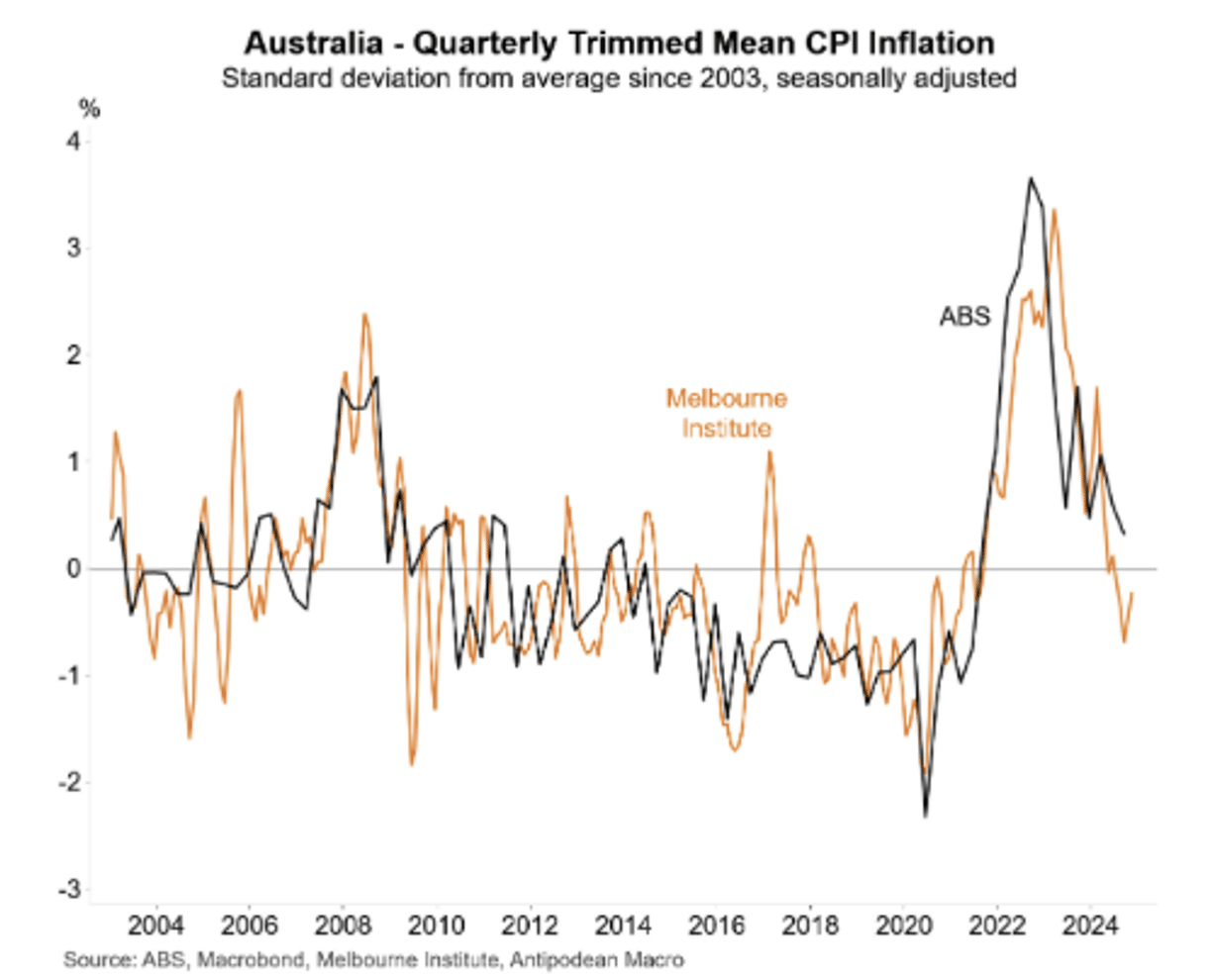

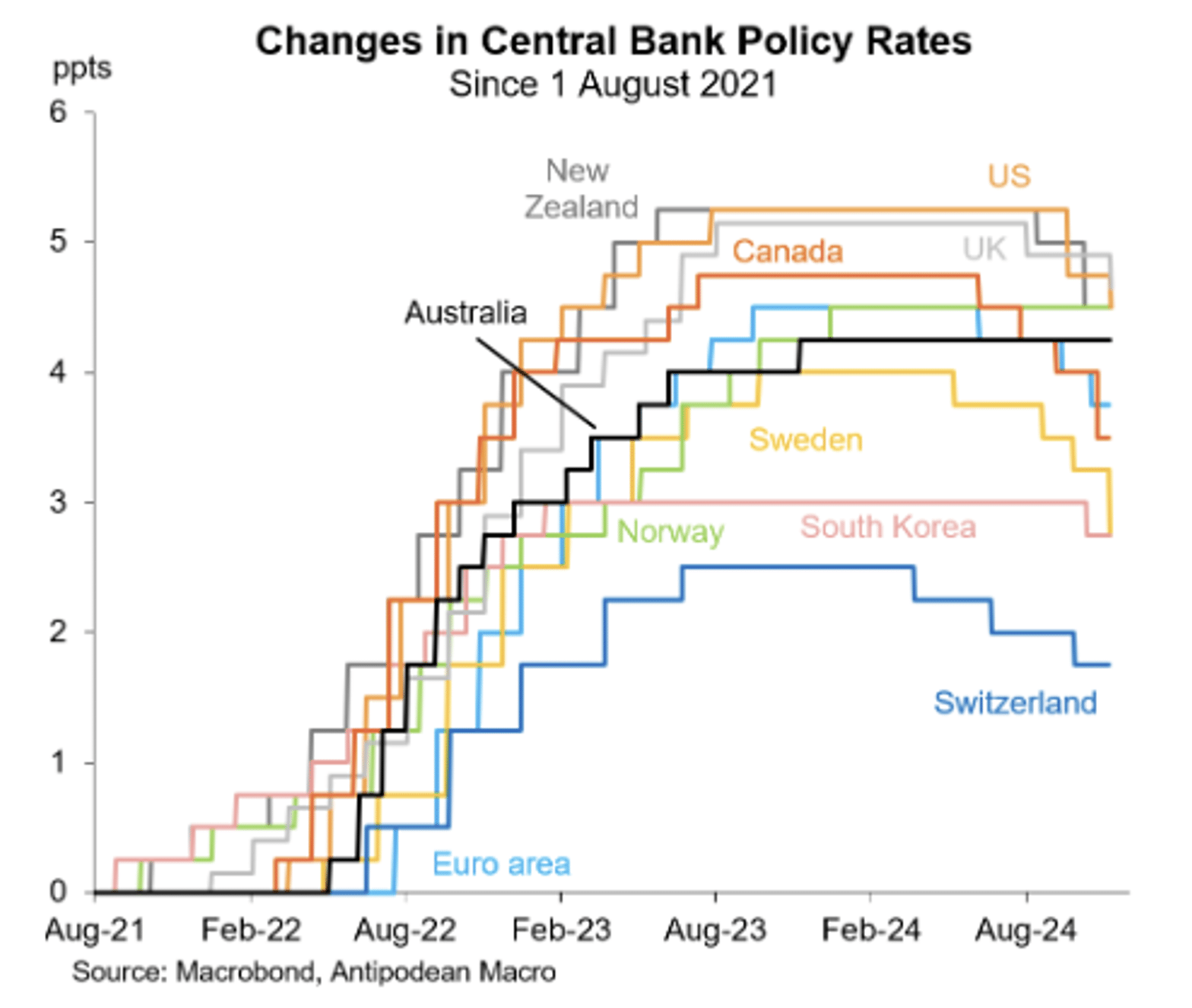

Global issues and the domestic inflation free-fall to spark further interest rate cuts

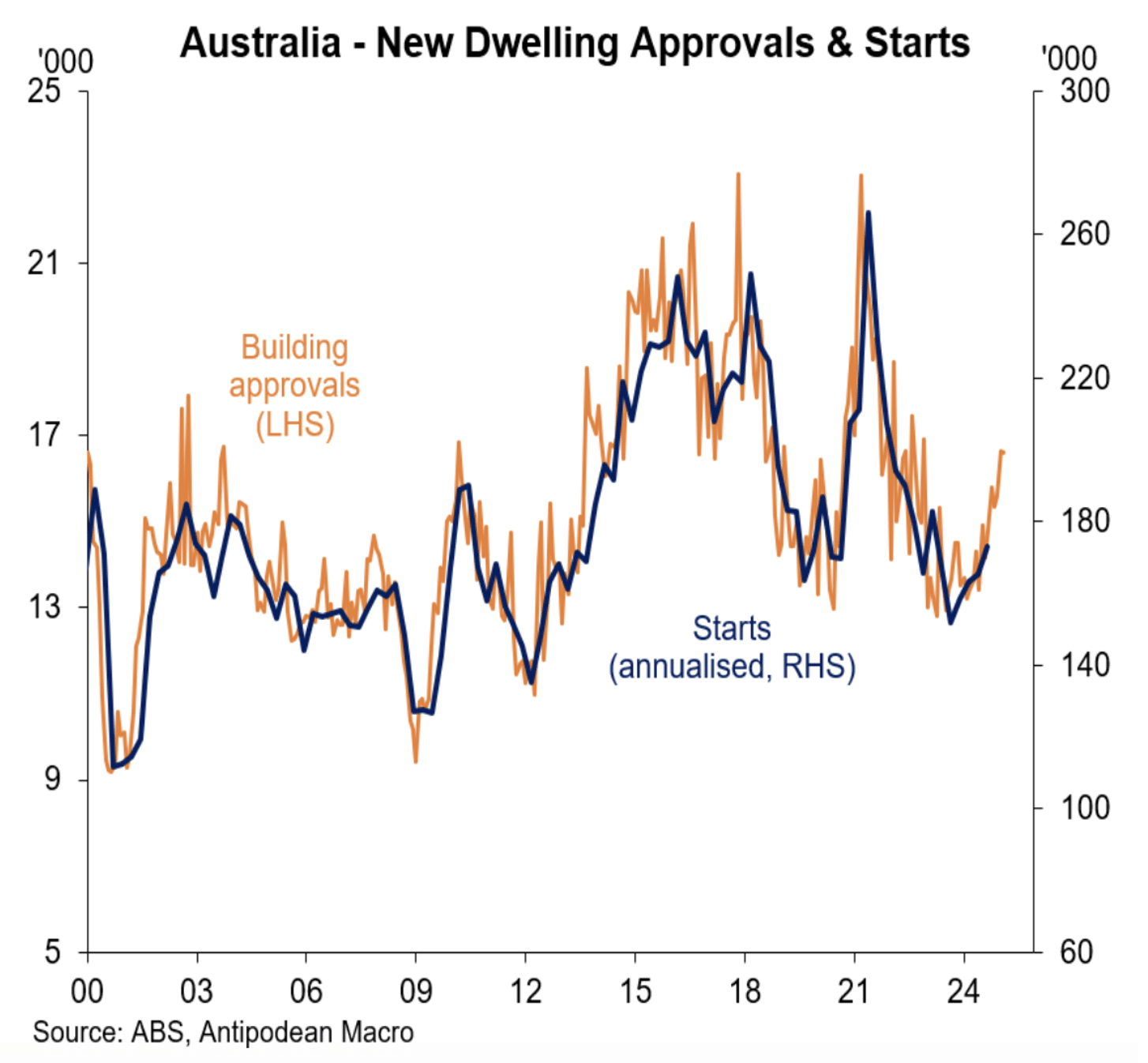

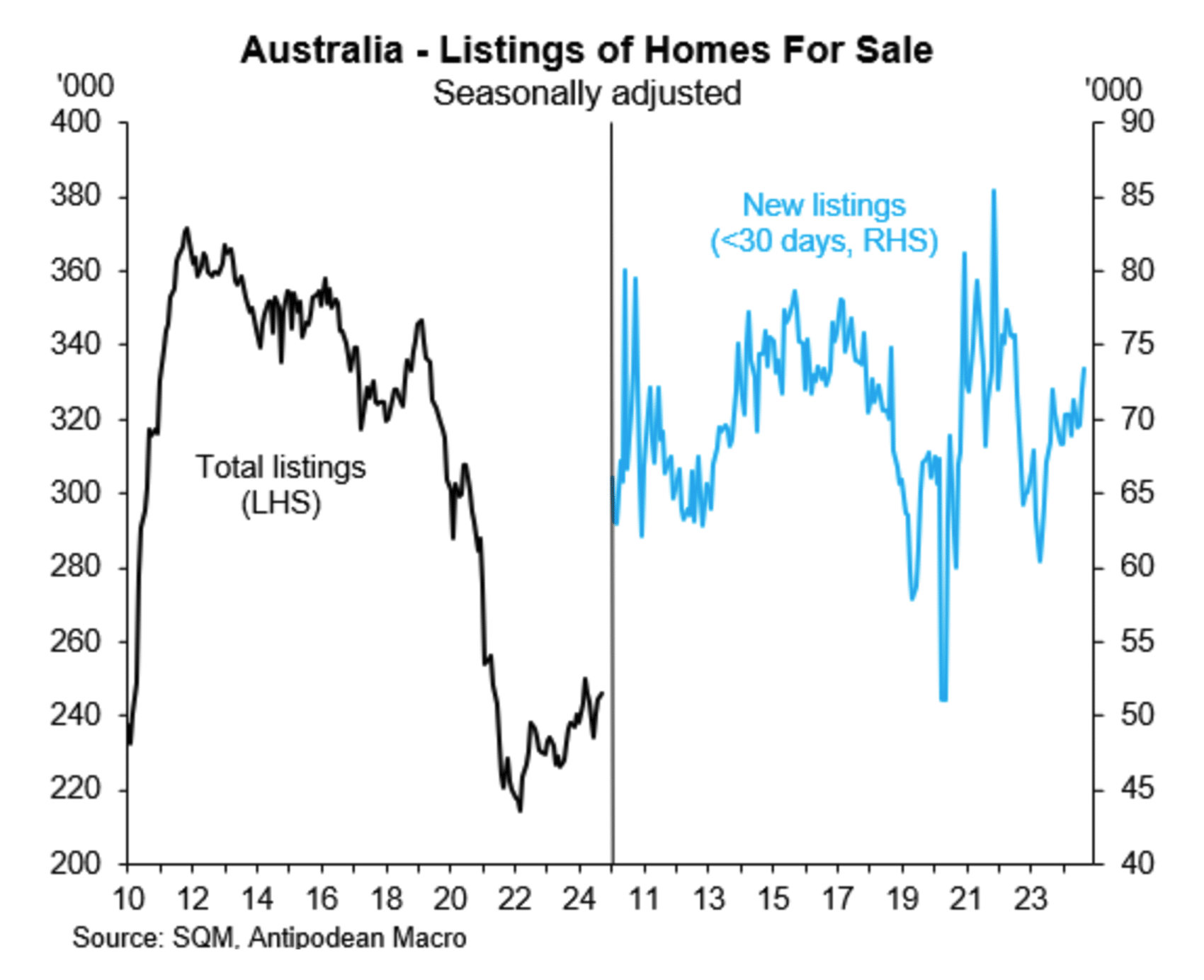

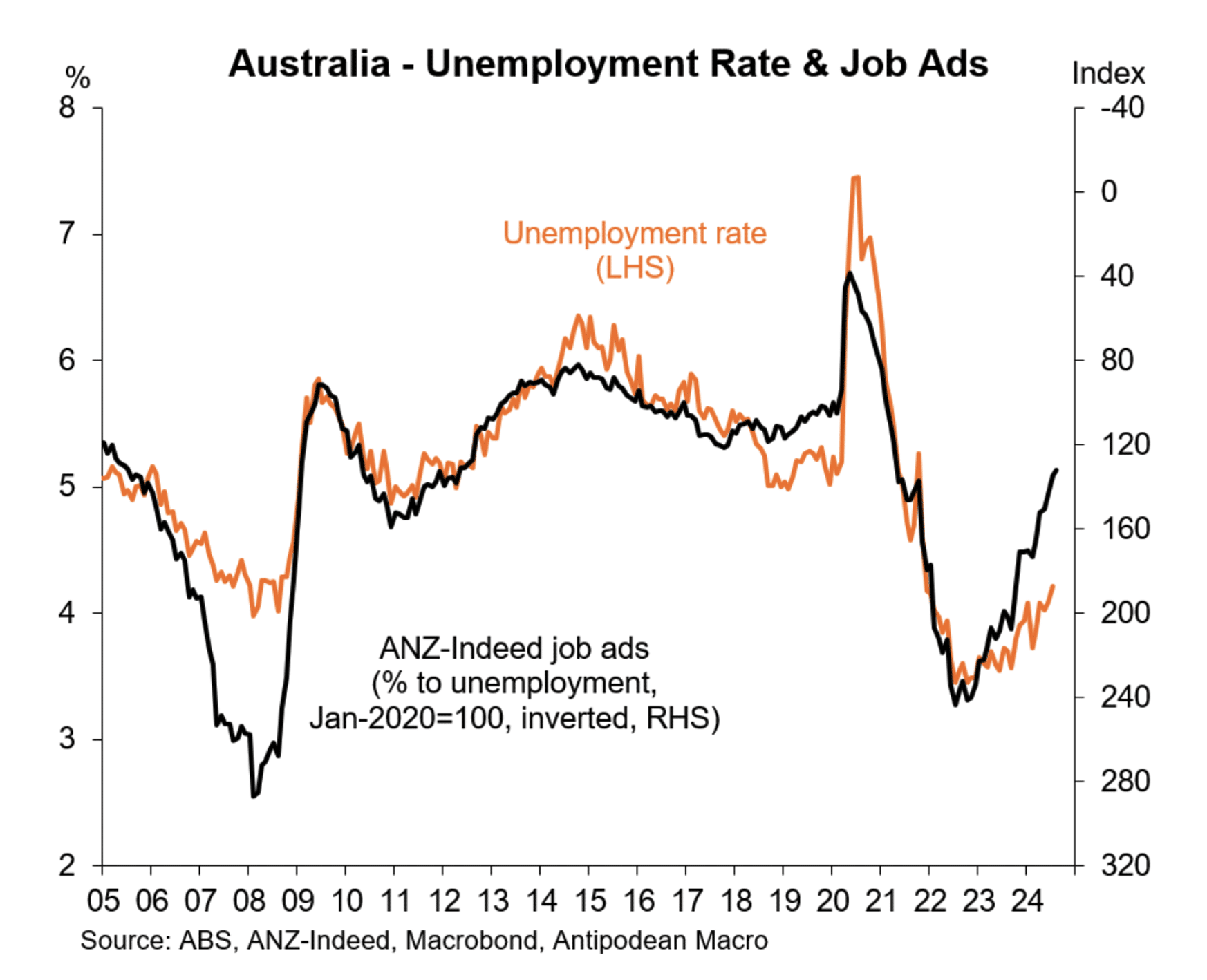

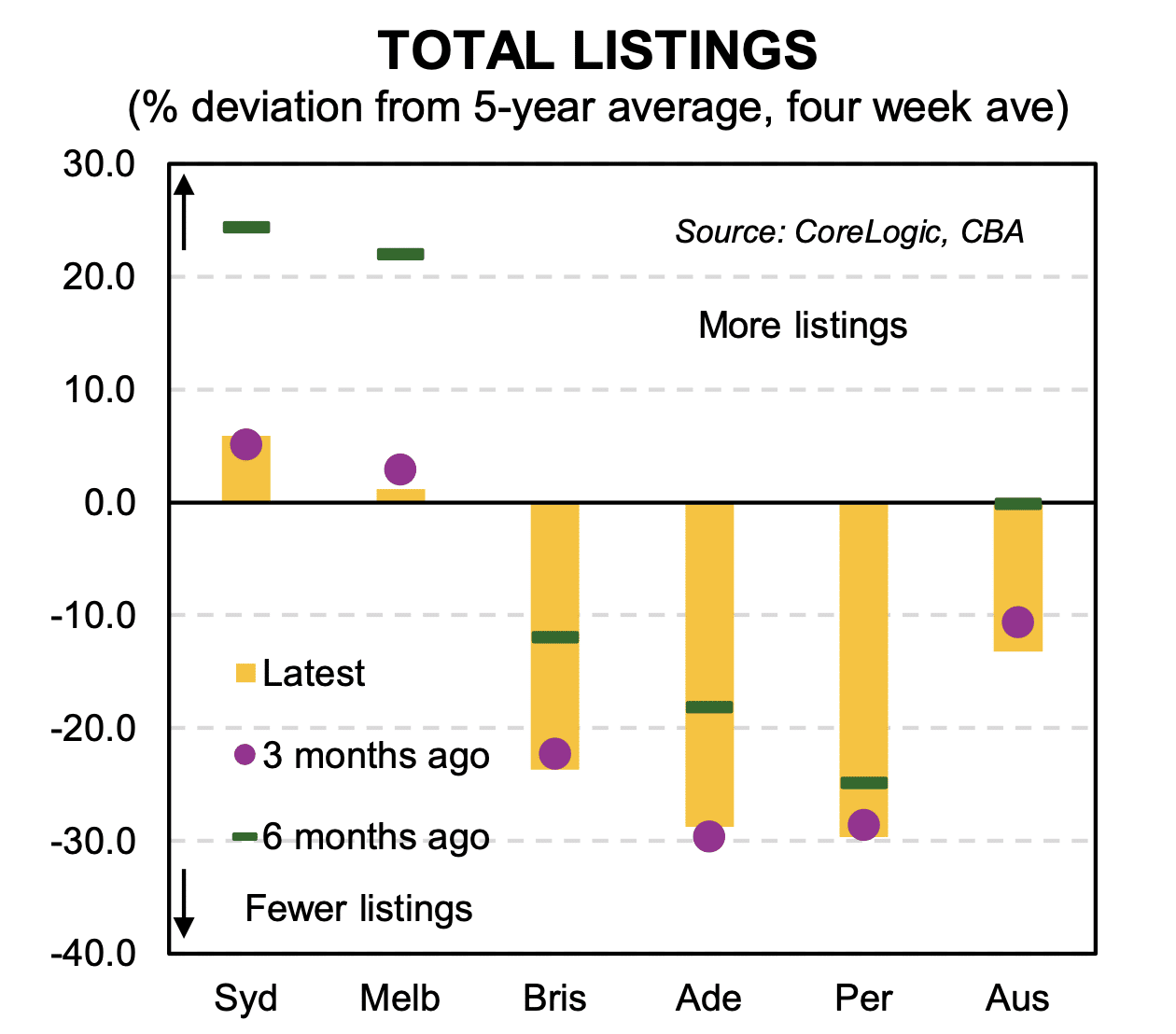

The moderate pick up in house prices in recent months is linked to a stalling in the growth of new supply, with new listings for sale falling and immigration inflows above official forecasts in the March quarter 2025. The resilient strength in the labour market has, for now, helped to support the housing market which has been further assisted by the early effects of lower interest rates.