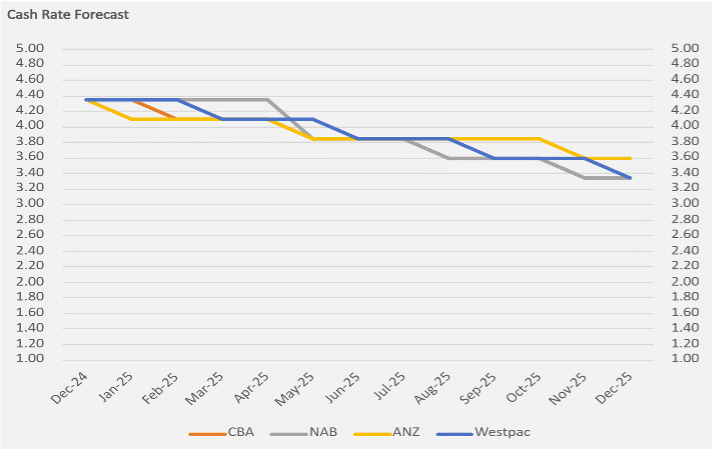

Official Cash Rate

Official Cash Rate

Inflation

Consumer Price Index

The Australian Bureau of Statistics (ABS) reported a 0.9% increase in the Consumer Price Index (CPI) for the March 2025 quarter, with a 2.4% annual rise – the same annual rate as December 2024, and the lowest since March 2021. As the quarter-on-quarter changes in the CPI from Q1 to Q4 2024 were 1.0%, 1.0%, 0.2% and 0.2% respectively, the most recent increase of 0.9% could be indicative of increased upward pressure on inflation. However, monthly figures show that while fluctuations are common, the overall trend in the annual inflation rate from March 2024 to March 2025 is downward. The rates were 3.5%, 3.6%, 4.0%, 3.8%, 3.5%, 2.7%, 2.1%, 2.3%, 2.5%, 2.5%, 2.4%, and 2.4%, indicating a general easing of inflation over the year despite some short-term variations. Most significantly, headline inflation rates from Q1 2024 to Q1 2025 were 3.6%, 3.8%, 2.8%, 2.4% and 2.4% respectively. These figures demonstrate an overall consistent easing of headline inflation, providing credibility for the RBA to achieve its sustained target of 2-3%.

This decline has been supported by price reductions in Recreation and culture (-1.6%), Furnishings, household equipment and services (-0.9%), Clothing and footwear (-0.8%) and Communication (-0.3%). It is also attributable to the ongoing implementation of government energy relief initiatives, where households have benefited from a temporary $300 federal energy rebate, alongside an additional $100 subsidy for Western Australia in FY24-25, easing financial pressures. These measures have driven a significant 11.5% drop in national electricity prices over the year to March. However, despite easing inflationary pressures, notable price increases were recorded in Housing (+1.7%), Education (+5.2%), Food and non-alcoholic beverages (+1.2%), Health (+2.9%) and Alcohol and tobacco (+1.2%). Meanwhile, the CPI data has had little impact on stock market volatility, with the ASX 200 experiencing corrections amid uncertainty over the U.S. trade war, prompting investors to shift towards more stable assets.

Population & Employment

Population

As of September 2024, Australia’s population reached 27.31 million, reflecting an annual increase of 484,000 people (1.8% growth rate). This rise is primarily driven by net overseas migration (NOM), which added 379,800 people, alongside a natural increase of 104,200.

At the state and territory level, demographic shifts vary significantly. New South Wales, Victoria, and Queensland continue to attract the largest shares of the population, with NSW reaching 8.51 million, Victoria 7.01 million, and Queensland 5.61 million. Growth in these states is largely concentrated in urban areas—Melbourne and Brisbane both recorded a 2.7% population increase in 2024. This urban expansion is expected to drive higher demand for residential and commercial property, boosting credit activity, particularly in real estate financing and infrastructure projects.

Regional areas have also experienced strong growth, fuelled by a decentralisation trend as more people seek affordable living options beyond major cities. This is evident in regional Queensland and New South Wales, which saw population growth of 2% and 1.4%, respectively, over the past year. While this shift presents new opportunities for private credit markets, lenders must adapt to diverse local economic conditions. The expansion of regional areas may heighten demand for tailored financing products but could also increase risk exposure in less-established markets.

Employment

As of April 2025, Australia’s labour market remained steady, with the national unemployment rate holding at 4.0%. Total employment reached 14.55 million, reflecting continued workforce stability, while the employment-to-population ratio stood at 64.2%. The participation rate saw a slight dip but remained firm at 66.9%, and underemployment edged down to 5.9%, suggesting improved job security. Monthly hours worked stayed consistent at 1.98 million, underscoring strong labour force participation and retention.

At the state level, New South Wales (NSW) recorded an unemployment rate of 4.1%, marginally above the national average. The state added 75,100 full-time jobs over the past year, reinforcing its economic growth. Similarly, Victoria and Queensland sustained their employment momentum, with Queensland benefitting from rising demand in construction and services. Nationwide, full-time employment increased by 15,000, while part-time roles grew by 17,500 in the past month, reflecting a gradual shift towards more flexible work arrangements.

Over the year, employment expanded by 307,400 people in trend terms, driven largely by growth in urban hubs like Sydney, Melbourne, and Brisbane. Migration patterns continue to shape housing and infrastructure demands, fuelling urbanisation and impacting real estate and private credit markets—especially in mortgage lending. However, the rise in part-time employment across multiple states suggests that while the overall job market remains stable, securing full-time roles remains a challenge, influencing household cash flow in certain sectors.

Despite these dynamics, the 2.2% annual increase in total employment and steady underemployment rate signal a resilient labour market, providing a stable foundation for credit risk management across both urban and regional economies.

Housing

Dwelling Approvals

For the year leading up to May 2025, Australia’s residential building approvals witnessed a notable decline. Total dwelling approvals fell by 8.8% month-over-month to 15,220, despite posting a 13.4% year-over-year increase. Private sector house approvals dropped 4.5% to 8,804, while approvals for private sector dwellings excluding houses saw a sharper 15.1% decline to 6,104. This downturn aligns with a broader trend of weakening residential building values, which fell 7.6% to $8.98 billion. In contrast, the non-residential building sector surged by 46%, reaching $6.61 billion in value. At the state level, the landscape was mixed—New South Wales (+19.6%) and Queensland (+5.8%) recorded gains, whereas Western Australia (-20.5%), Victoria (-31.6%), South Australia (-11.9%), and Tasmania (-42.2%) experienced substantial declines in total dwelling approvals.

Despite the downturn in approvals, the housing construction sector showed signs of recovery, with residential construction value rising 1.5% in the December quarter to $23.75 billion, marking the highest quarterly figure in three years. This increase reflects stabilising borrowing and building costs, hinting at a potential resurgence in residential investment. However, persistent challenges—particularly trade labour shortages and capacity constraints—continue to weigh on the sector. While growth remains evident, the overall market outlook remains cautious, with some economists forecasting modest gains in FY2025.

Zooming out to national trends, dwelling approvals remain subdued, extending a three-year pattern of underperformance. The sluggish pace stems from deep-rooted planning challenges, exacerbated by bureaucratic delays and widespread community opposition to development. According to the Property Council, only 47% of NSW councils are meeting their residential development assessment processing targets, and just 171,394 new homes were approved nationwide in 2024—far below the 240,000 annual approvals needed to meet the National Housing Accord’s goal of 1.2 million new homes by 2029.

Compounding these issues, high interest rates, elevated land prices, and rising construction costs have dampened developer activity. However, potential policy tailwinds—such as fast-tracked development approvals—could offer relief. The NSW Government has introduced a five-year housing completion target for 43 local government areas, spanning Greater Sydney, Illawarra-Shoalhaven, Central Coast, Lower Hunter, and Greater Newcastle, with a broader statewide target of 377,000 new homes by 2029 under the National Housing Accord. These initiatives aim to foster the development of more diverse, well-located housing in areas with existing infrastructure capacity, such as transport and water services, supported by financial incentives and infrastructure funding to help councils meet their targets.

Median Dwelling Price

By April 2025, Australia’s housing market had settled into a more consistent upward trend, with the national median dwelling price rising 0.7% over the last quarter, reaching a new high of $$820,331. However, growth across the country remained uneven, with individual states and territories experiencing varying levels of expansion.

As of April 2025, Sydney retained its position as the nation’s most expensive market, with its median house price climbing to $1.191 million, reflecting a .04% increase over the quarter. Despite this modest rise, prices in Sydney have largely stabilised since the market plateaued in early 2025, and they are expected to remain relatively steady throughout the remainder of the year.. Nationally, dwelling values rose by 0.7% in the March quarter, driven by moderate to strong performances in all states, while Hobart saw a slight decline of 0.4%.

The total value of residential dwellings across Australia climbed to $11 trillion, though the mean dwelling price dipped slightly to $976,800. Rising land prices are reshaping buyer preferences, pushing demand toward more affordable regions and away from high-cost metropolitan areas such as Sydney, where land prices now surge pass $2,000 per square meter. Despite a broader slowdown in growth, demand remains strong in Perth and Brisbane, largely driven by affordability and shifting demographic trends.

Vacancy Rates

Australia’s national rental vacancy rate has undergone a significant shift, with the latest data from April 2025 revealing an increase to 1.6%—a minimal jump from 1.5% the previous year. Melbourne, Adelaide and Canberra saw the sharpest rises, with its vacancy rate climbing 0.4 percentage points over the last year, while Perth continues to record the lowest vacancy rate at just 1%. Despite these increases, the overall vacancy rate remains well below the 3% threshold typically associated with a balanced market.

Migration continues to fuel demand, keeping Australia’s rental market under sustained pressure. The tight supply of rental properties is expected to persist, particularly in high-demand urban areas. Although vacancy rates are rising, they remain far from ideal for renters, meaning affordability challenges are unlikely to ease. For private credit markets, persistently low rental vacancy rates signal ongoing demand for housing, reinforcing investor confidence in real estate-backed lending. However, affordability constraints and rising interest rates could pose challenges, particularly for borrowers with high leverage.

House Rental Rates

Australia’s rental market has experienced a significant slowdown, contrasting sharply with the rapid growth of the past four years. Rental price increases across capital cities have largely plateaued or even declined in some areas. The latest data reveals just a 1.7% quarterly growth across combined capital cities—a notably subdued pace compared to previous years—while annual gains stand at 3.5% for houses and 4.6% for units. Although rental conditions have eased somewhat, supply remains constrained in many cities, perpetuating a landlord’s market. National rental yields have held steady at 3.7%, though regional areas continue to deliver stronger returns, driven by more robust rental growth and slower price increases.

From a renter’s perspective, Sydney’s rental market remains in crisis, plagued by severe undersupply, exceptionally low vacancy rates, and relentless demand fuelled by population growth and rising construction costs. While there are signs of stabilisation, rents continue to climb, with average weekly house rents reaching $781—painting a grim picture for tenants. A vacancy rate of just 1.9% has intensified competition for available properties, further exacerbating the scarcity of rental housing. Several factors have contributed to this crisis, including surging construction costs, a limited pipeline of new housing projects, and restrictive regulations that have deterred investors. Additionally, the influx of skilled immigrants and international students has heightened demand, pushing rental prices to record highs and straining an already limited housing supply.