Amid rising rates, global tariffs and persistent market volatility, private credit is gaining attention as investors search for defensive allocations.

‘Turbulent’ is how many investors define the month that was.

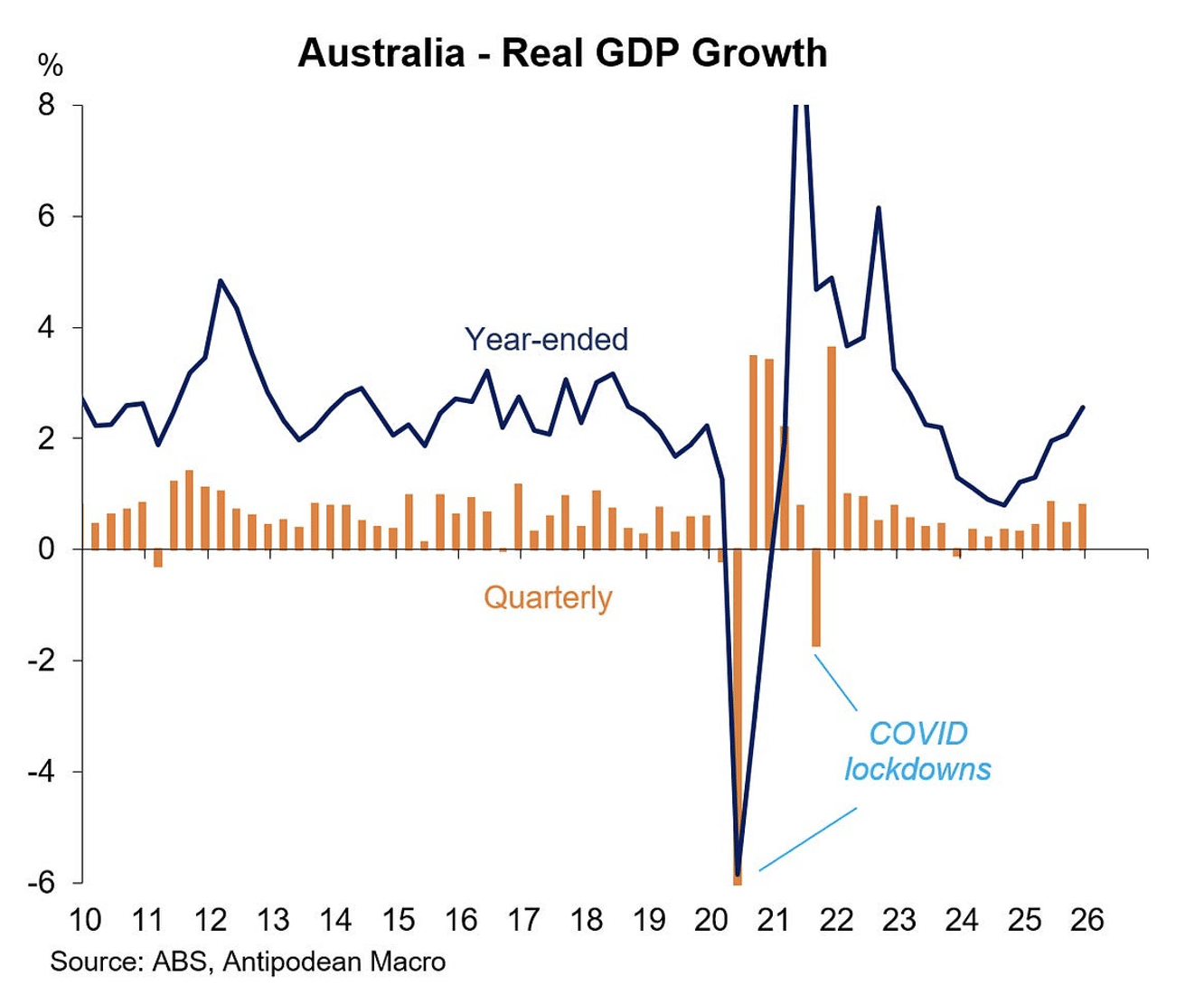

Locally, the Reserve Bank of Australia (RBA) passed on a rate rise due to stubborn and accelerated inflation, while, globally, Trump surprised with 15 per cent global tariffs, significantly higher than anticipated. Coupled with ongoing geopolitical tensions, persistent market volatility, and uncertain macro conditions, many investors are spooked.

The hunt is on for defensive allocations and safe haven assets, particularly those underpinned by stable, well-regulated economies. In this context, Australia’s ‘Goldilocks’ economy, defined by our AAA credit rating, lender friendly environment, and world-class judiciary and legislative system, continues to demonstrate resilience in the face of global disruption.

Complementing these fundamentals is the persistent growth of our local private credit market. Australia’s private credit market is now valued at $224 billion, growing nine percent year-on-year. Real estate private credit, in particular, is forecast to reach $92 billion by 20291.

Amidst global market shocks, Australian real estate private credit has come of age. Delivering reliable, risk-adjusted income, defensive characteristics, and proven performance across market cycles, investors are rightly paying attention.

In a rising rate environment, the benefits are even more pronounced with investors expecting healthier returns due to the floating rate nature of private credit investments. For sophisticated investors, real estate private credit has become a core part of well-diversified portfolios.

Will the tailwinds continue?

With record growth, many question whether Australian real estate private credit can continue to deliver. The dynamics of our property market provide confidence that tailwinds are only strengthening.

Australian real estate has enjoyed 20 years of sustained growth, with the residential market now surging past $12 trillion in value2. Yet, despite decades of development, housing construction is failing to close the current shortfall, estimated at 200,000 to 300,000 dwellings3, let alone keep pace with Australia’s booming population. Growing by approximately 400,000 people annually4, new supply continues to lag structural demand – a gap that official forecasts suggest will persist, and likely widen, over the next 12 months5.

Amidst this housing supply crisis, we are seeing a pullback from traditional lenders as regulation and capital constraints mean construction lending is often too complex or cumbersome for big banks.

Put simply, the market can’t keep pace with demand. To seize the opportunity, borrowers need a capital partner with proven expertise that can provide flexible, bespoke loan terms, and who is responsive, reliable, and specialised. A true partner understands the underlying transaction and can work collaboratively to help deliver the best project outcomes on time and on budget.

This is especially important in a rising rate environment, where developers may experience margin shrinkage on projects. Delivering the right project, in the right market, at the right price is critical to success.

For investors, choosing a credible, specialist investment manager means access to these bank-grade borrowers who are proactively choosing private credit, securing strong returns without taking on additional risk.

At Zagga, we have financed over $2.5 billion in projects with more than 50 percent of our bank-grade borrowers returning to us to finance their next project. Importantly, we have repaid in excess of $1.5 billion to our investors across more than 200 successful exits, and an average annual return of 9.2 percent6.

Focus on the 3 Ts

Today, real estate private credit accounts for ~26 percent of residential development finance in Australia7. In contrast, more established markets, like the US, see private credit represent up to 50 percent of construction funding. As tailwinds strengthen, there is clear growth potential for this asset class in Australia.

However, real estate private credit is a vast and varied asset class, and not every investment opportunity is created equal. Robust due diligence is key to realising the sector’s potential, with the 3 Ts providing a solid framework for investors:

1. Transparency

A credible manager should provide investors with transparency of information, easy access to detailed data, and clear, comprehensive reporting and disclosures. At Zagga, all investors have access to our executive team to further bolster confidence and credibility.

2. Track Record

Defaults are a natural feature of any lending transaction; they do not automatically translate into losses. What ultimately determines outcomes is risk management – the quality of underwriting, the strength of structuring, and the experience with which recoveries are managed to secure the best outcome for both investors and the borrower. A cycle-tested manager understands recovery processes, maintains strong counterparty relationships, and can act decisively to protect investor capital. This is where governance and discipline translate directly into returns.

3. Trust

Proven expertise across market cycles, consistent performance, and specialist knowledge and capabilities build trust between manager, investor, and borrower. It is important to choose a manager who is not only delivering returns today, but has demonstrated ability to navigate uncertainty, operate with transparency, and act with integrity when conditions tighten.

'Perfect panacea'

After a turbulent month, investors are looking beyond public markets to protect and diversify portfolios, without sacrificing returns. Australian real estate private credit could prove the perfect panacea to calm market nerves. Backed by solid economic fundamentals, fuelled by unprecedented growth tailwinds, and underpinned by credible, specialist investment managers this asset class is yet to realise its full potential. Crossing your Ts will ensure you’re well placed to seize the opportunity.

1. Alvarez & Marsal, Australian Private Debt Market Review, November 2025

2. Cotality, November 2025 – https://www.cotality.com/au/insights/articles/monthly-housing-chart-pack—november

3. National Housing Supply and Affordability Council (NHSAC), State of the Housing System 2025; various industry estimates placing the current cumulative shortfall in the 200,000–300,000 range.

4. Australian Bureau of Statistics, National Population Statistics, 2025.

5. National Housing Finance and Investment Corporation

6. Average investor return across the active portfolio as at 31 December 2025. Past performance is not a reliable indicator of future performance.

7. Alvarez & Marsal, Australian Private Debt Market Review, November 2025

This article was developed in collaboration with Zagga, a Stockhead advertiser at the time of publishing and additionally published in The Daily Telegraph, NT News, The Cairns Post, Geelong Advertiser, Gold Coast Bulletin, The Mercury, Adelaide Advertiser, Toowoomba Chronicle, The Courier Mail and the Townsville Bulletin.

This article does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions.