The earlier cautious optimism about an economic recovery is translating to confirmation about broader economic strength.

While serious uncertainties dominate the global outlook amid elevated geopolitical threats to markets and economic activity, particularly in the Middle East, the domestic drivers of the economy are broadly positive.

A combination of prior interest rate cuts, moderate fiscal stimulus and an increase in commodity prices have helped to spark the more positive tone.

While the good news of a solid recovery in GDP and productivity is welcome, there remain concerns about the sustainability of these trends in a climate where monetary policy is restrictive. Indeed, inflation remains above target which is posing a policy challenges for the RBA. As a result, it retains an inclination to further increase interest rates, following its February rate hike, but the timing and extent of future interest rate movements is uncertain.

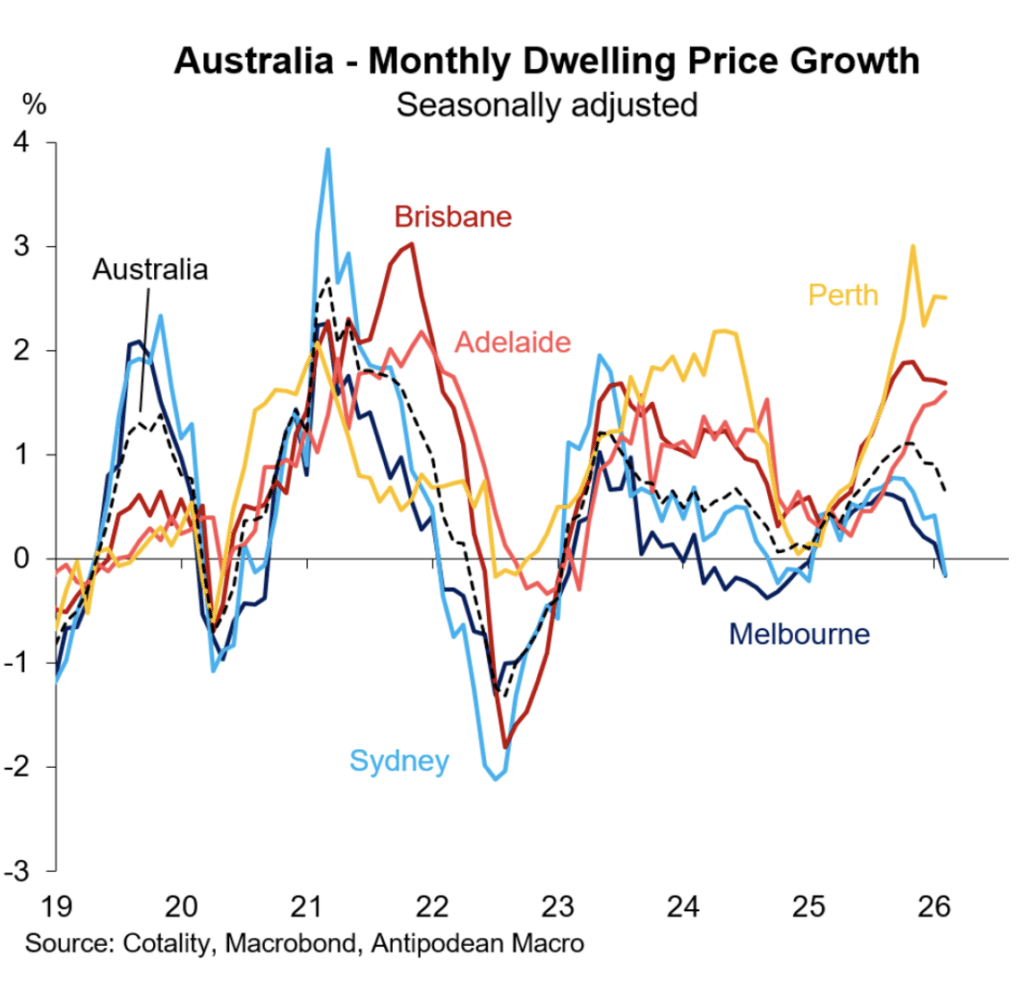

House prices are rising but at a slower pace than was seen in the middle of 2025. Prices in Melbourne and Sydney are weak, but remain very strong in Perth, Adelaide and Brisbane.

Key data

Below is an update of key trends in the economy over the past month:

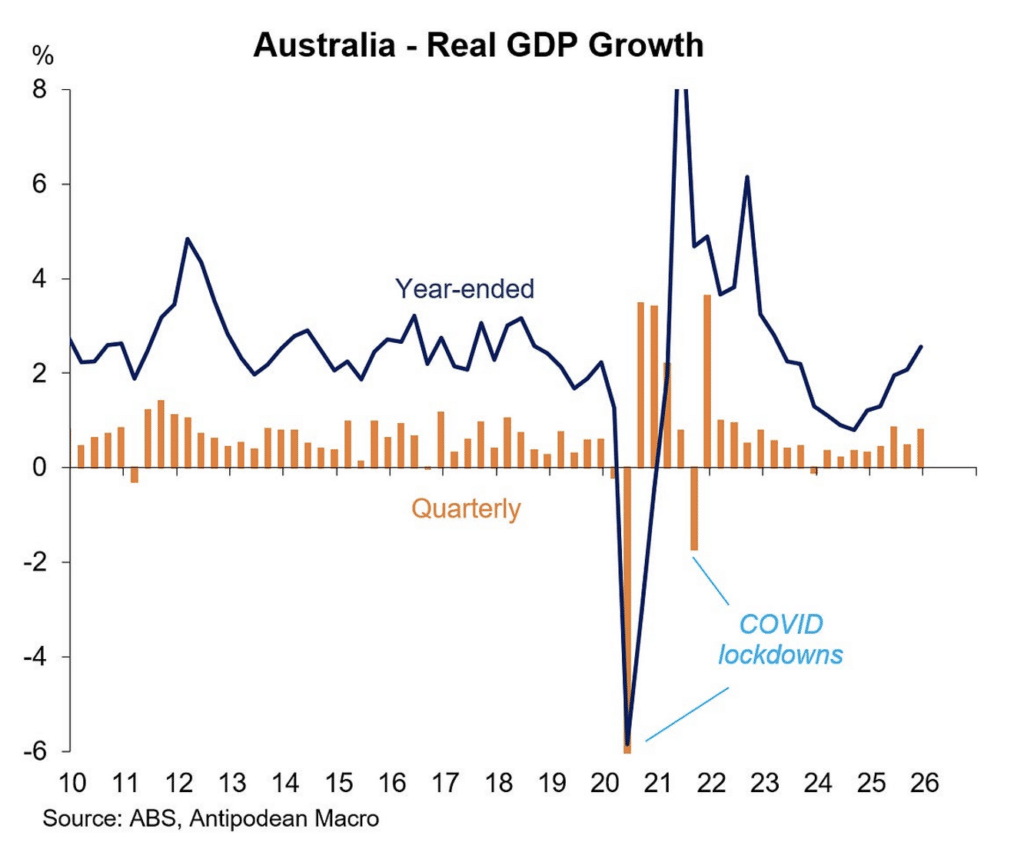

- GDP rose a solid 0.8 per cent in the December quarter to be 2.6 per cent higher than a year earlier. The annual rate of GDP growth was the strongest in 3 years and builds on the broader economic recovery evident since late 2024. The composition of economic growth was favourable – in annual terms, household spending was up 2.4 per cent, business investment was up over 4 per cent, while government demand growth slowed to 3 per cent as public projects came to an end and the effects of a slight tightening in government spending continued to impact. Net exports subtracted from GDP as import volumes rose strongly.

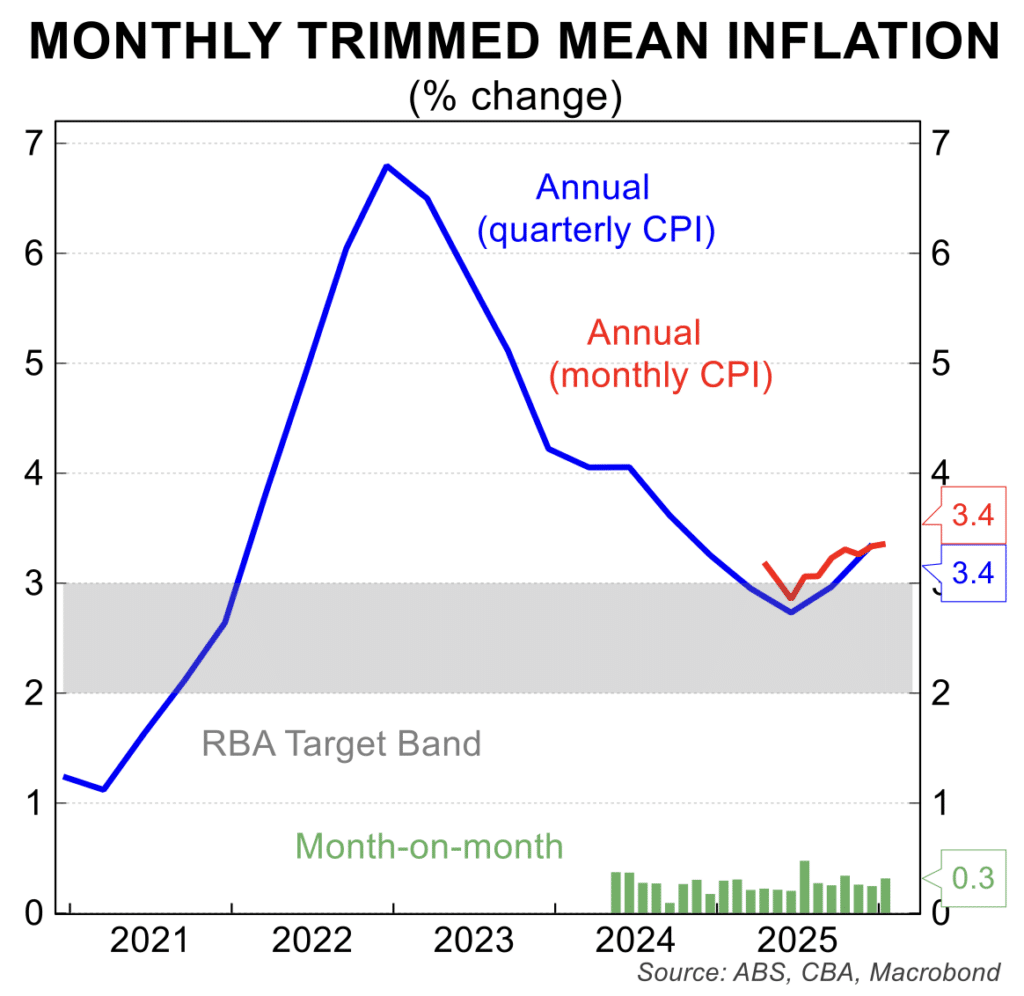

- Inflation rose 3.8 per cent in the year to January, with the trimmed mean rate edging up to 3.4 per cent. The ending of electricity subsidies, an unseasonal rise in international travel costs, housing and clothing costs added most to annual inflation. Inflation remains above the RBA target although it has signalled it would prefer to see the quarterly inflation data (next due 29 April) as the main input to its interest rate deliberations.

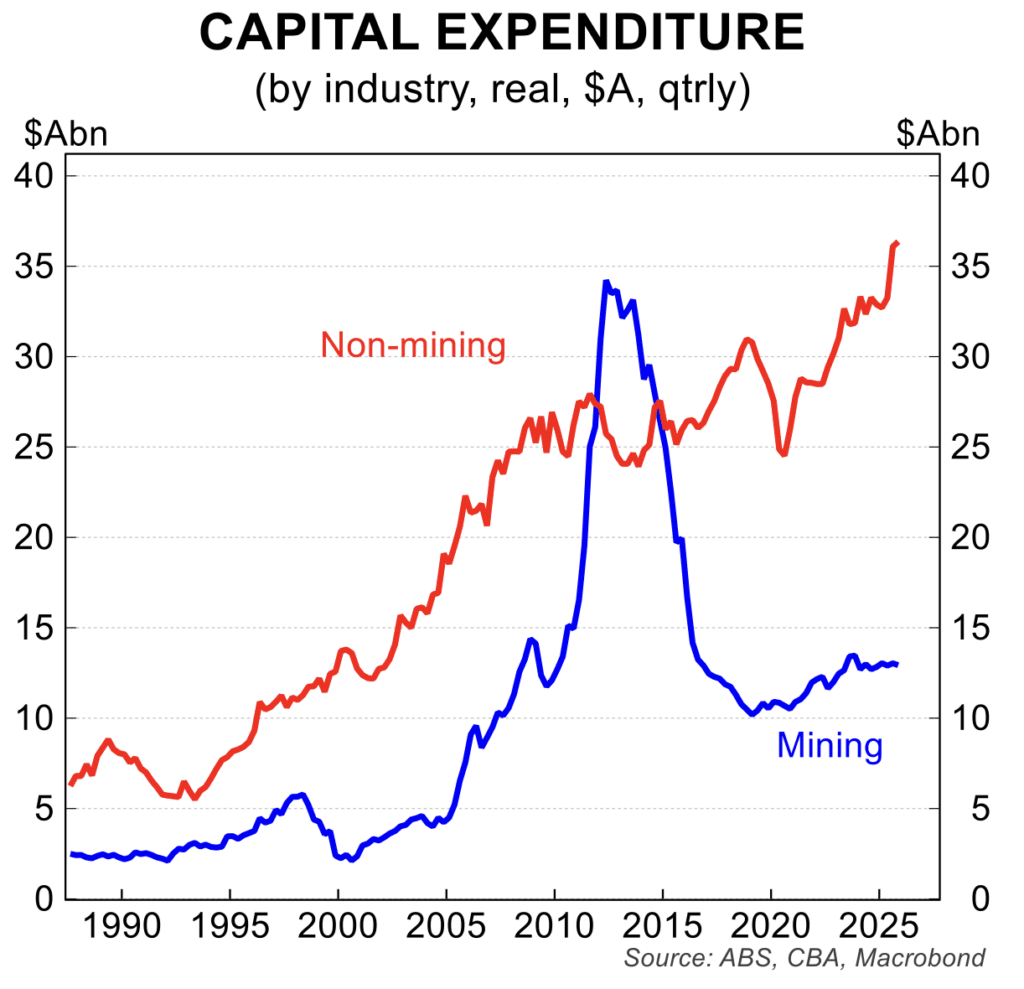

- Private sector business investment rose 0.4 per cent in the December quarter after jumping 6.4 per cent in the September quarter to lock in a solid upswing in capital expenditure. Encouragingly, non-mining investment is driving the recovery which is an important element in delivering a much-needed increase in productivity (the red line in the chart below). Businesses expect capital expenditure to rise a further 7 per cent in FY2026-27.

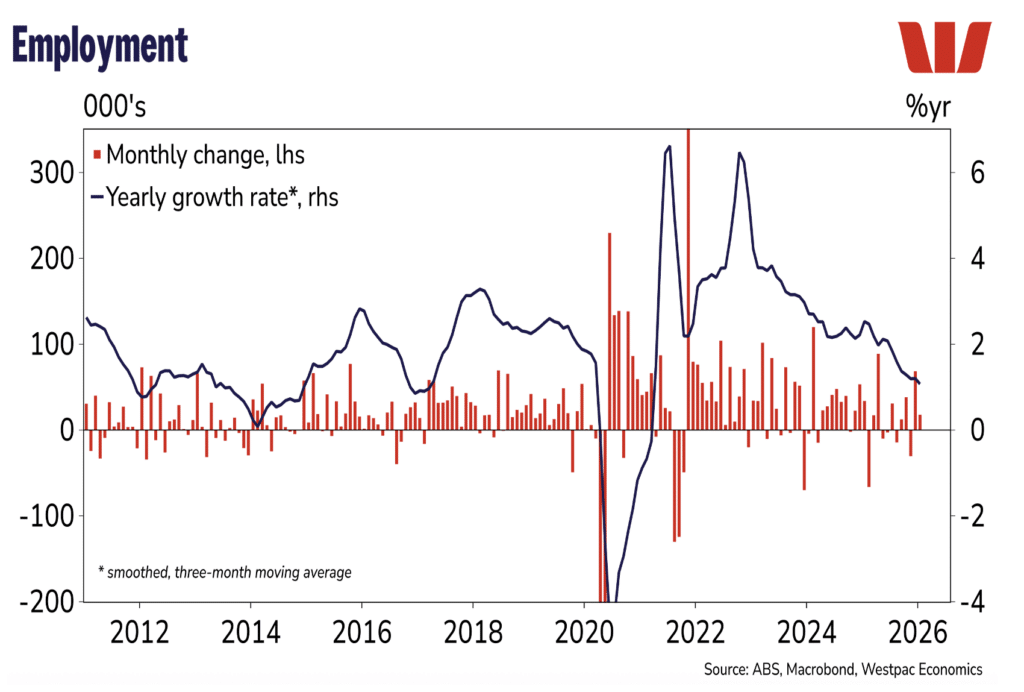

- The unemployment remained at 4.1 per cent in January, confirming a turning point lower after a period of rising unemployment through 2024 and most of 2025. Employment growth was a moderate 18,000 in January which saw the annual increase in employment slow to 1.0 per cent, the slowest yearly increase in almost a decade (the black line in the chart below). Of note and as a sign of a cooling in labour market conditions, the workforce participation rate and the employment to population ratios have both fallen sharply over the past year.

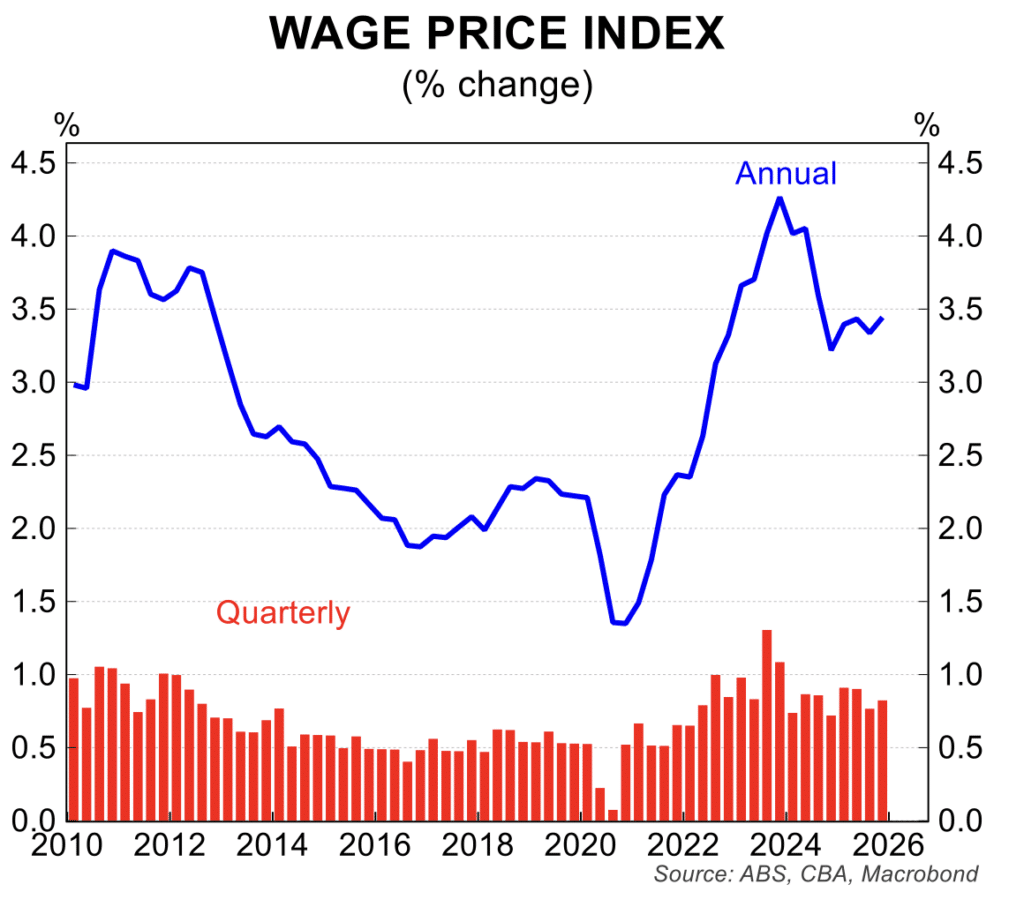

- The wage price index rose 0.8 per cent in the December quarter for an annual increase of 3.4 per cent. The annual rise in wages has been between 3.25 and 3.5 per cent for the past year, which is down from the peak of 4.25 per cent in late 2023 and early 2024. The current wage dynamics are consistent with inflation tracking around the mid-point of the RBA’s 2 to 3 per cent target. The wages data are also consistent with a moderation in the labour market conditions.

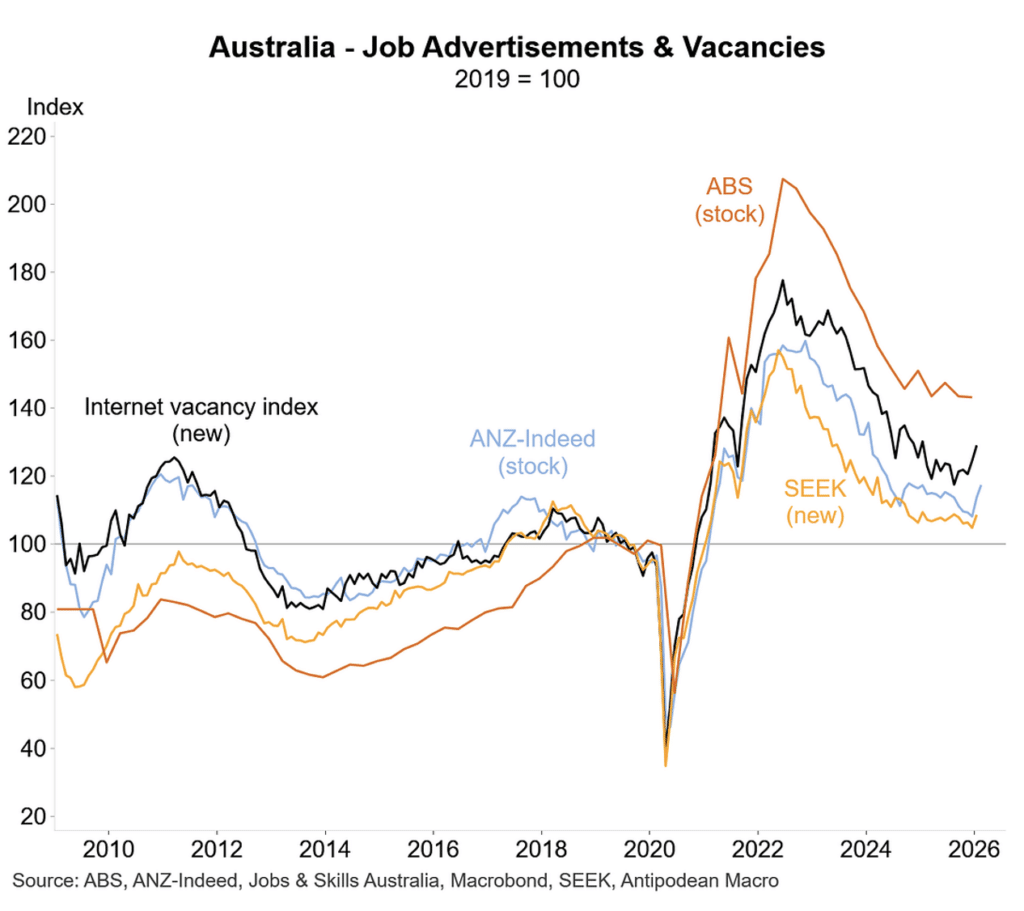

- The number of job vacancies and advertisements have edged higher in recent months, in line with the broader economic recovery. This follows a two year period where there were sharp falls in labour demand. At current levels, the job vacancies data point to steady jobs growth and a slight rise in the unemployment rate over the next half year.

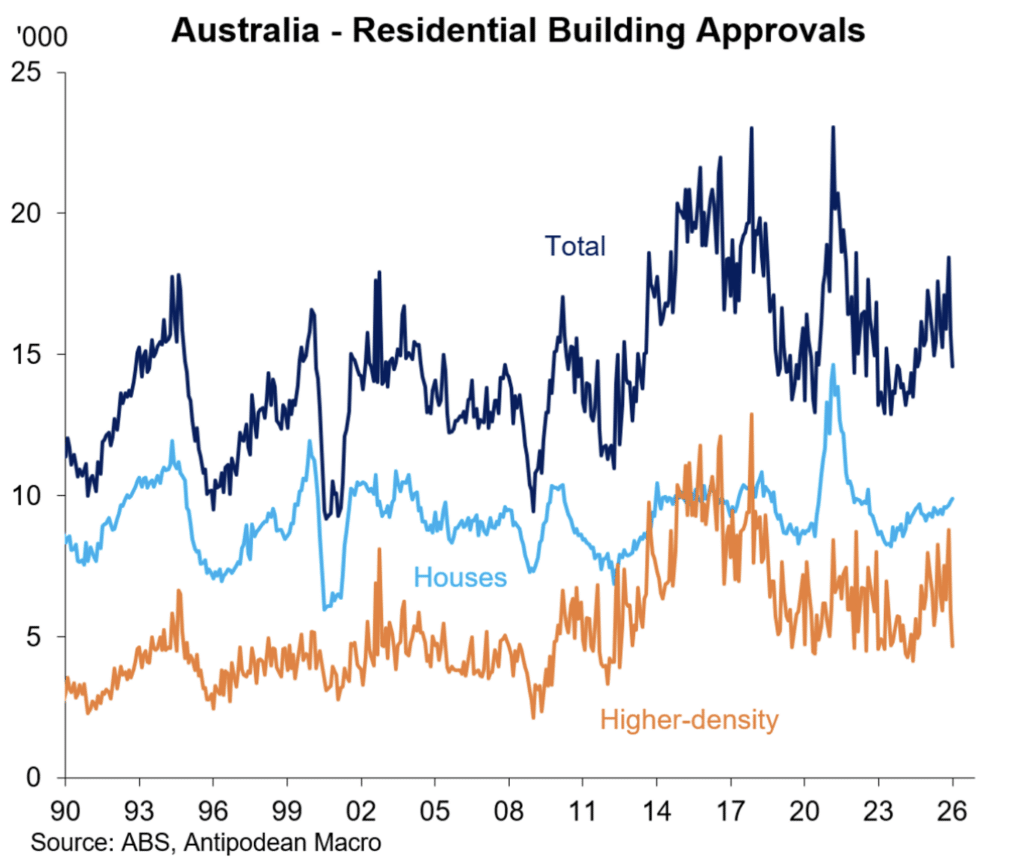

- The number of new building approvals has been very disappointing in recent months. Residential approval fell 7.2 per cent in January which brought the cumulative fall since September 2025 to 15 per cent. After an encouraging lift in approvals through the bulk of 2025, the recent decline will hold back much needed supply, which is a critical factor in helping to deal with housing affordability. There is little chance of the government meeting its target for 1.2 million new dwellings in the 5 years to 2029. A figure closer to 1 million is more likely.

RBA monetary policy and the current market pricing for the cash rate

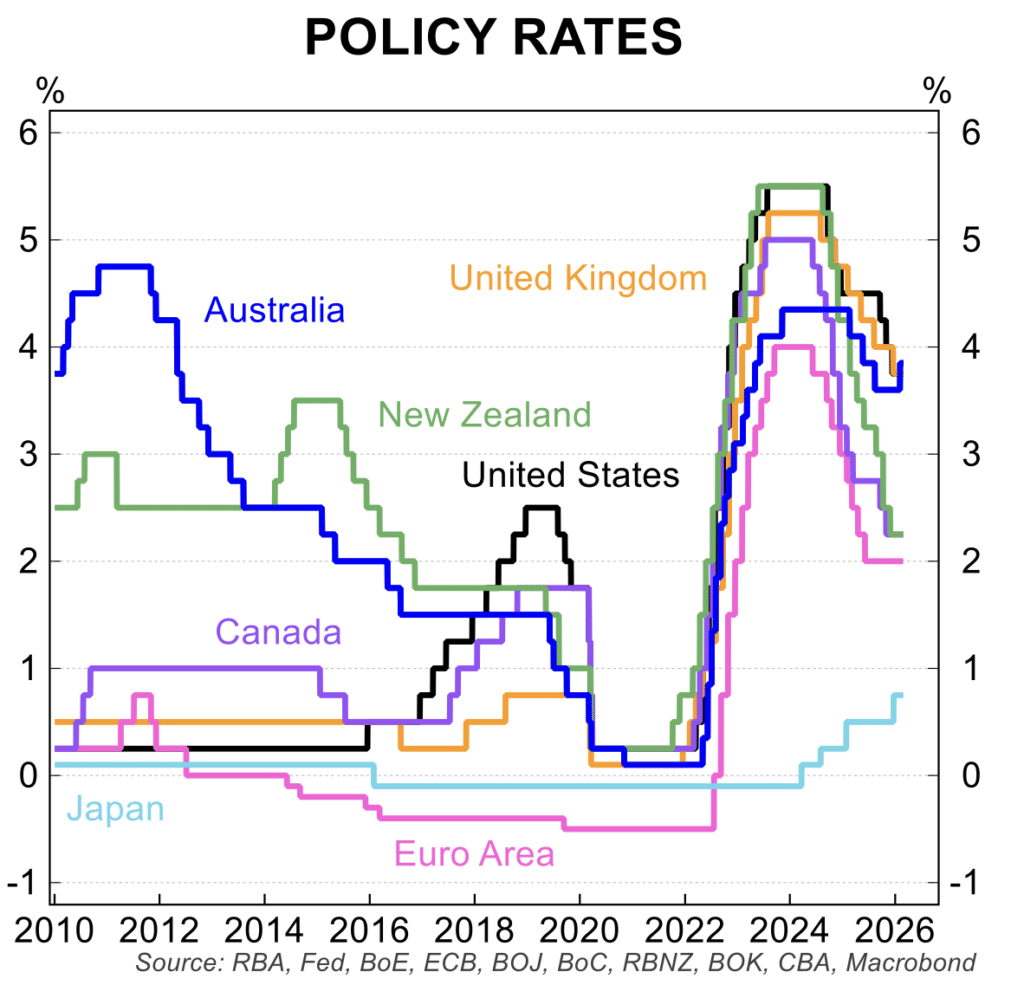

The RBA hiked interest rates in February in reaction to the upside surprise in inflation and due to the more positive tone of private sector demand. While RBA Governor Bullock continues to avoid giving guidance on the outlook for monetary policy, markets are pricing in a peak cash rate of 4.25 per cent in 2027 from the current 3.85 per cent rate. Market pricing can be volatile and can move with new information. The current global uncertainties will have significant implications for monetary policy.

Monetary policy settings overseas remain caught between ‘on hold’ or the ‘possibility of further cuts’, especially in the US and UK. The near-term inflation and economic growth momentum will determine whether the relative calm can be sustained.

House prices

There remains a major divergence in house price trends across Australia.

Over the last three months, prices in Melbourne and Sydney have fallen, while prices in Perth, Adelaide and Brisbane have risen strongly, by 4 to 6 per cent, for annual increases of 22 per cent in Perth and 17 per cent in Brisbane.

The divergence in price pressures is linked to State-by-State issues, largely linked to demand from population growth, but also the addition to supply from new construction. In Victoria, for example, dwelling construction has been strong for the best part of a decade, a fact that accounts for part of its relatively weak prices not just recently, but over the past decade or so.

In aggregate, there remains a major shortage of dwellings relative to demand, as issue that will only be resolved when there is a sustain increase in construction and a period of slower population growth or some combination of the two.

There are no material changes to the rental market – it remains very tight in most cities. This has seen rents re-accelerate to well above wages growth, which will dampen household spending in the medium term. It does, however, provide a boost for investors who are taking advantage of a more favourable rental yield and the relative ease of finding an occupant.

Stephen Koukoulas is Managing Director of Market Economics, having had 30 years as an economist in government, banking, financial markets and policy formulation. Stephen was Senior Economic Advisor to Prime Minister, Julia Gillard, worked in the Commonwealth Treasury and was the global head of economic research and strategy for TD Securities in London.