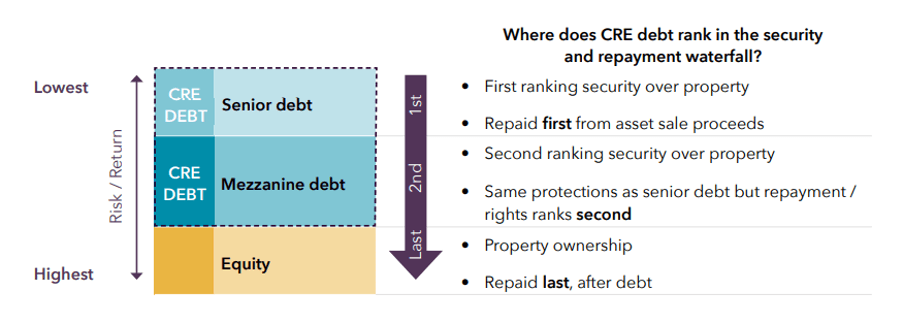

Figure 1: The CRED repayment waterfall

Figure 1: The CRED repayment waterfall

Private credit can avoid the volatility often seen in public markets for products such as bonds – which are extremely sensitive to interest rate movements and sentiment – instead, providing

Looking for higher returns and diversification? Dive into alternative real estate investments in Australia – discover new opportunities & explore how Zagga can help you build a stronger portfolio.

Unlock attractive returns in the Australian commercial real estate market. Explore debt opportunities, market trends, and how Zagga can help investors achieve their financial goals. Contact us today!