• Property dominates Australia's household wealth

• Private credit is a complement to traditional bank lending

• Zagga offers income via secured property investments

Special Report: Australia’s $12 trillion property obsession is now driving the rapid rise of private credit as investors look for income without owning bricks and mortar.

Australia’s favourite asset isn’t listed on the ASX. It’s the thing people live in, argue over at auctions, and quietly trust as their financial foundation long after the dinner table conversations have ended.

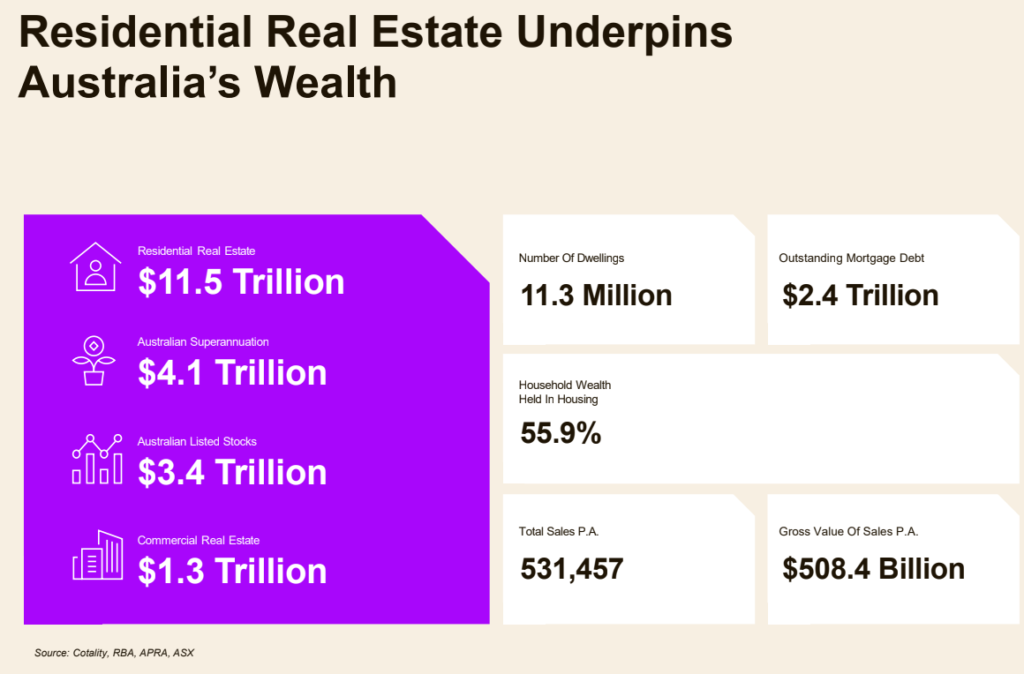

Today, the residential property market is worth more than $12 trillion – much larger than the size of the Australian sharemarket – with about 55% of household wealth tied up in bricks and mortar.

In many ways, this isn’t just a market statistic. It’s a reflection of how deeply property is embedded in the Australian psyche, not just as shelter, but as the central pillar of personal wealth.

But as bank capital and traditional funding pathways tighten up, developers have shifted toward alternative sources of finance that are more bespoke, specialised, and can structure deals more flexibly.

This has accelerated the rise of Australia’s private credit market, which has shifted from a niche alternative into a significant force within the country’s financial system.

According to Alvarez & Marsal’s 2025 review, the private credit market now stands at $224 billion in assets under management, growing far faster than traditional bank and bond markets.

Around $92 billion of this capital is tied directly to commercial real estate-related lending, signalling how closely private credit has become intertwined with the property sector itself.

This is the environment in which Sydney-based Zagga operates.

Turning a national obsession into structured income

Tom Cranfield, executive director of risk and execution at Zagga, knows all too well that property in Australia is a well-loved asset.

“Australia’s property market is now valued at approximately three times the ASX,” he said. “For many, it’s aspirational to own their home. It’s the largest asset that most people have on their balance sheet.”

And what has become more evident is the sheer scale of that asset class and the structural imbalance within it.

Strong population growth and persistent undersupply in major metropolitan markets continue to drive reliable demand for new housing and development finance.

Australia’s $12 trillion property market is helping fuel the rise of private credit as investors seek income beyond bricks and mortar. Pic: Getty Images.

From Cranfield’s perspective, that dynamic creates a more stable environment for credit investors, where risk can be assessed against real assets and genuine buyer demand rather than short-term price speculation.

“For private credit, it’s showing that there is some really good downside protection for our investments, and that the asset class should be low in volatility.”

Zagga’s focus on build-to-sell residential and infill developments in established metropolitan areas reflects this logic.

These projects operate in active, buoyant markets with visible buyer demand and defined exit options.

Rather than chasing capital gains, Zagga’s strategy centres on generating stable income through secured lending, with returns linked to contractual structures.

A different way to express belief in property

Cranfield sees real estate private credit as a practical pathway for investors who already believe in Australia’s long-term property fundamentals, but want to express that belief through property-linked income without becoming landlords – no borrowing, no tenants, no maintenance, and no exposure to the ups and downs of a single asset.

“If you think that the eastern seaboard of Australia, and particularly the major metropolitan areas, is a good place to make a return on your capital then investing with Zagga gives you conservative exposure to the real estate sector with attractive risk-adjusted returns,” he said.

Instead of taking on the operational, transactional and leverage burdens of owning property, investors gain access through secured lending, where capital is backed by underlying assets.

One key difference, Cranfield emphasised, is accessibility.

Zagga’s minimum investment for wholesale or sophisticated investors is $100,000, allowing entry into real estate-backed exposure without the deposits, stamp duty and ongoing costs that accompany direct property ownership.

Defensive by design

For Zagga, consistency is structural to the strategy.

“I think that our investment strategy is there to be a defensive strategy to achieve those core pillars that I keep talking about: consistency, safety, stability,” Cranfield noted.

The Zagga flagship Feeder Fund, established in 2019, has operated through rapid rate increases, inflation shocks, supply chain disruptions and changing macro conditions.

Across that period, the fund has continued to meet its return hurdles, reinforcing its positioning as an income-focused strategy designed to perform through the full property cycle, not just in favourable markets.

“I think time will always separate a disciplined manager from one who’s chasing returns.”

Structural, not opportunistic

While private credit often gains attention during periods of tighter bank lending or market volatility, Cranfield views its role as far more permanent.

He believes real estate private credit has become a structural component of modern financial markets rather than a temporary response to dislocation.

“It’s absolutely structural. In fact, I think it’s structural and sustainable,” he said.

For investors, it offers a way to convert Australia’s vast property market into a deliberate income strategy rather than a speculative play.

“I also believe investors appreciate the opportunity to have a stable part of their portfolio that produces a consistent, income generating return,” he said, adding that he is not a registered financial advisor.

This article was developed in collaboration with Zagga, a Stockhead advertiser at the time of publishing and additionally published in Adelaide Now, Cairns Post, The Courier Mail, The Daily Telegraph, Geelong Advertiser, Herald Sun, NT News, The Chronicle, The Mercury and Townsville Bulletin.

This article does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions.