Stephen Koukoulas opens his March update following another interest rate increase from the Reserve Bank of Australia (RBA), with rates rising for the second consecutive month. The February and March hikes have now taken the Official Cash Rate (OCR) to 4.1%, with inflation firmly at the centre of the RBA’s decision‑making.

RBA hikes again amid inflation concerns

Stephen notes that inflation had already been “a little uncomfortable” for the RBA even before the recent oil shock. Higher oil and petrol prices are now feeding mechanically into inflation, raising questions about how long those effects may last.

There is debate around whether these pressures will reduce if oil prices fall back and supply conditions normalise — something the RBA itself has acknowledged. But for now, with inflation and the economy running too hot, another rate hike was deemed necessary.

Early‑2026 data disappoints

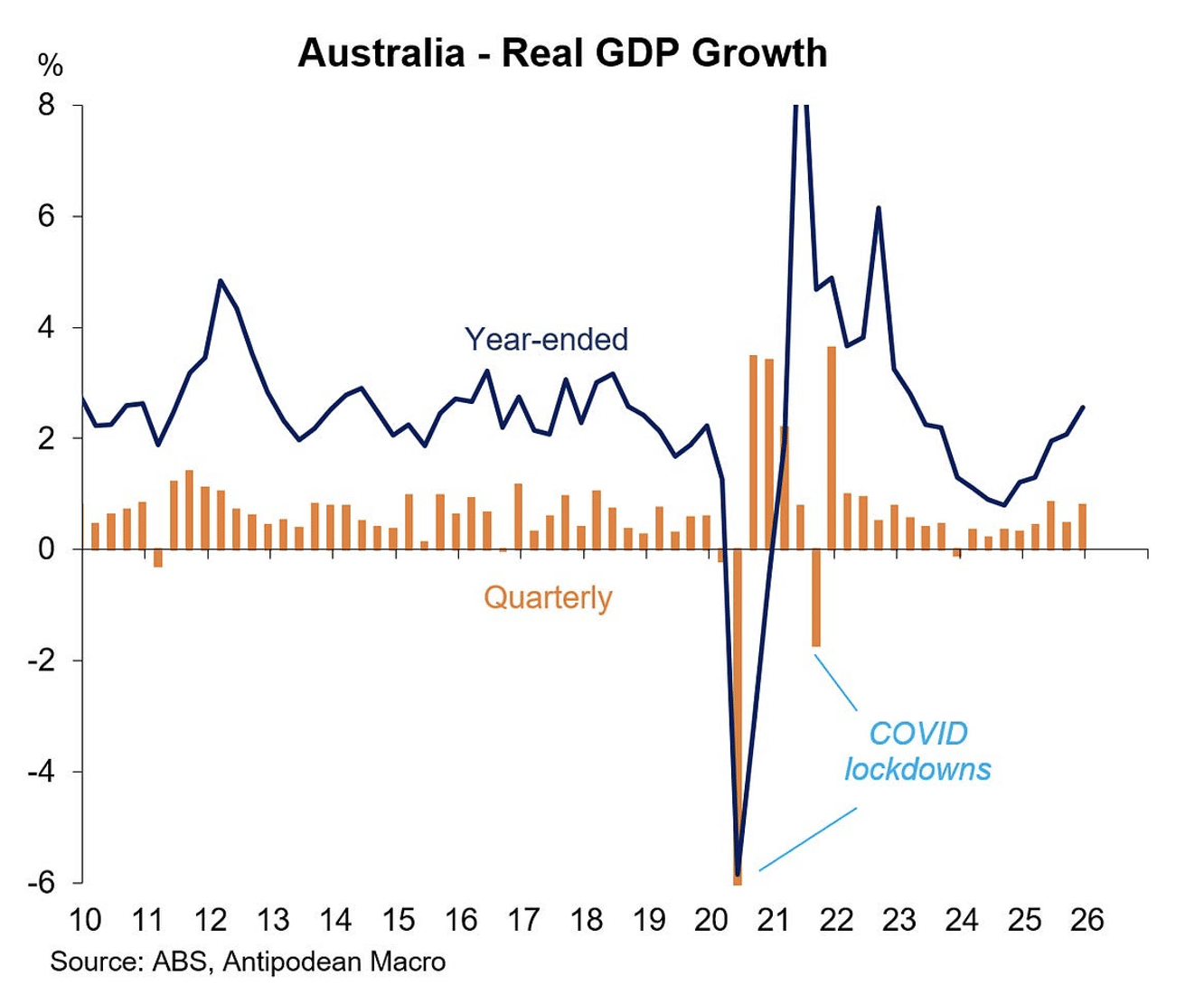

While GDP growth through the end of 2025 was strong, Stephen says the tone has shifted in early 2026, with a range of indicators suggesting momentum is starting to falter.

Household spending has weakened materially. Spending was negative in December, rose only slightly in January, and internal bank data points to another very weak outcome in February. It seems, consumers are “hunkering down” under higher inflation, while wages growth remains moderate, limiting income growth and constraining activity.

Building approvals fall back

Another area of concern is housing construction. Stephen says optimism around a construction upswing has faded, with building approvals now 15% lower than September levels.

While approvals — particularly for apartments — have been volatile month to month, Australia remains well short of the roughly 20,000 approvals per month needed to approach the government’s 1.2 million‑dwelling target. Instead, current approvals are hovering closer to 15,000–16,000 per month, meaning the housing shortage is likely to persist.

Housing market mixed, rentals tight

House price conditions remain volatile. Sydney and Melbourne are weak, with prices flat to slightly down, while Perth, Brisbane and Adelaide continue to record strong gains — although momentum is beginning to slow.

Rental vacancy rates remain low, and demand has been supported at the lower end of the market by the first‑home‑buyer 5% deposit scheme.

Some brighter spots remain

Stephen highlights a few encouraging developments. Productivity — long a “bugbear” for the economy — is starting to lift from a low base. Business investment is also ticking higher, which is important for longer‑term growth. He cautions, however, that further rate hikes risk crimping this progress.

Focus turns to the Federal Budget

Attention is now turning to the Federal Budget on 12 May. Stephen notes expectations that the budget will be reform‑focused, including tax reform, tighter control of government spending, and a reduction in the budget deficit — potentially even a return to surplus.

If delivered, he says these measures would help take some of the steam out of the economy and support longer‑term stability.

The bottom line

The economy is navigating a difficult phase of tightening financial conditions, global uncertainty, and uneven domestic momentum. As Stephen puts it, the challenge now is getting the economy through this interest‑rate‑tightening phase “sooner rather than later.”

Watch the full video below:

Stephen Koukoulas is Managing Director of Market Economics, having had 30 years as an economist in government, banking, financial markets and policy formulation. Stephen was Senior Economic Advisor to Prime Minister, Julia Gillard, worked in the Commonwealth Treasury and was the global head of economic research and strategy for TD Securities in London.