SMSF ADVISER

Australia’s SMSF sector is growing at a record pace. With 14,500 SMSFs originated in the September quarter, the highest establishment rate in recorded history, SMSFs now control

AUSBIZ

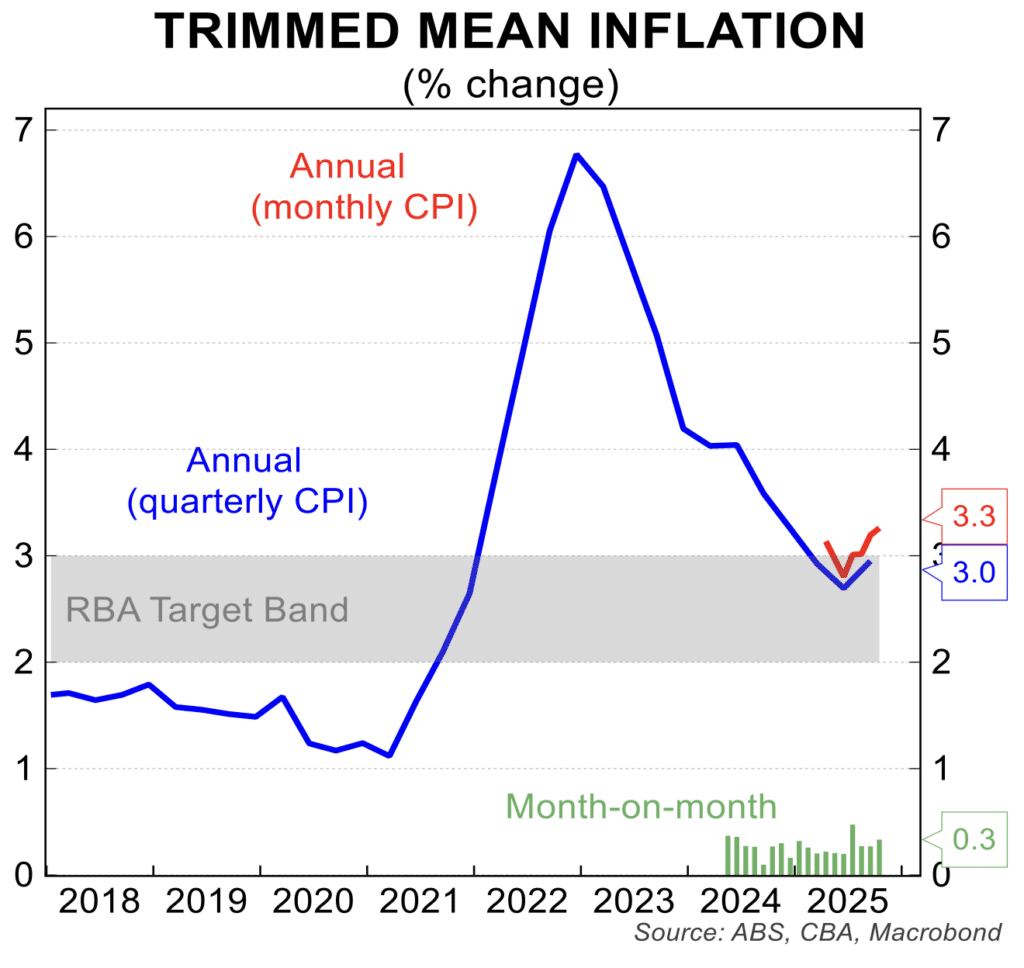

In this recent interview with Ausbiz, Alan Greenstein, Zagga CEO & Co-Founder argues Australia may experience stagflationary pressures, with inflation and interest rates rising while growth slows, yet

STOCKHEAD & THE AUSTRALIAN

With market twists and turns, investors searching for reliable income are increasingly turning their attention to real estate private credit. When the world feels this