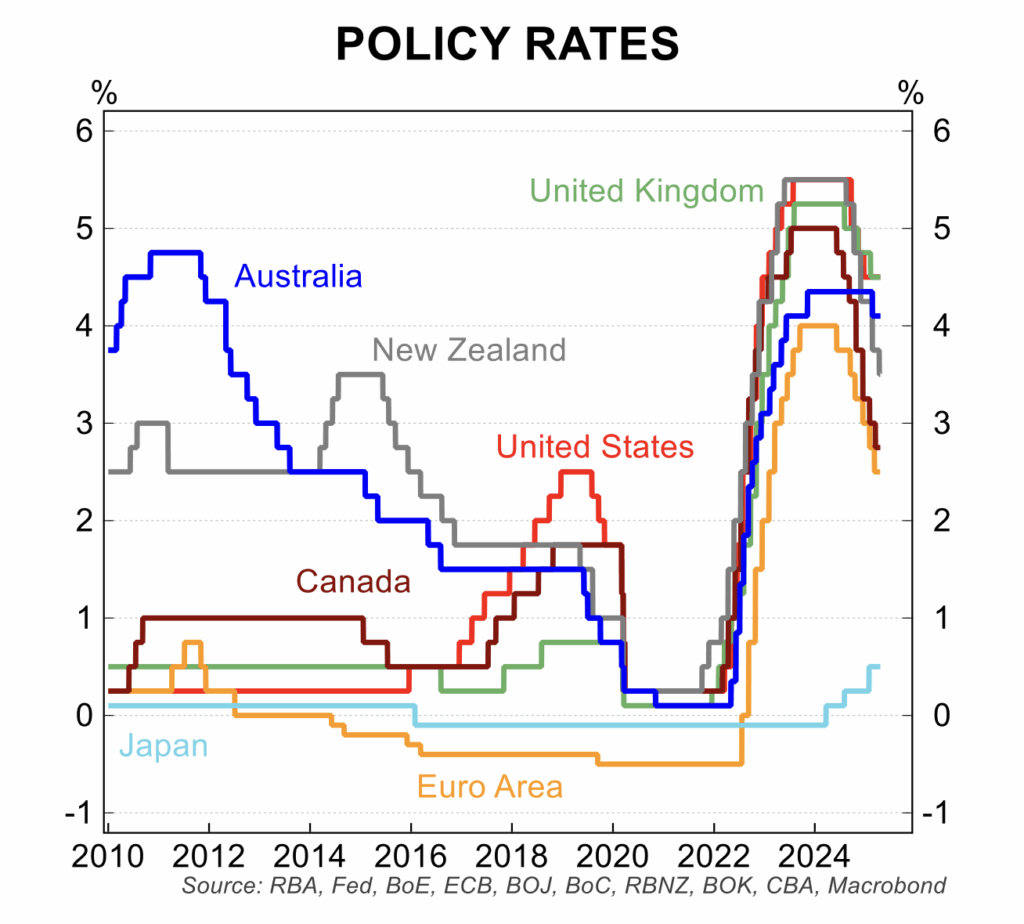

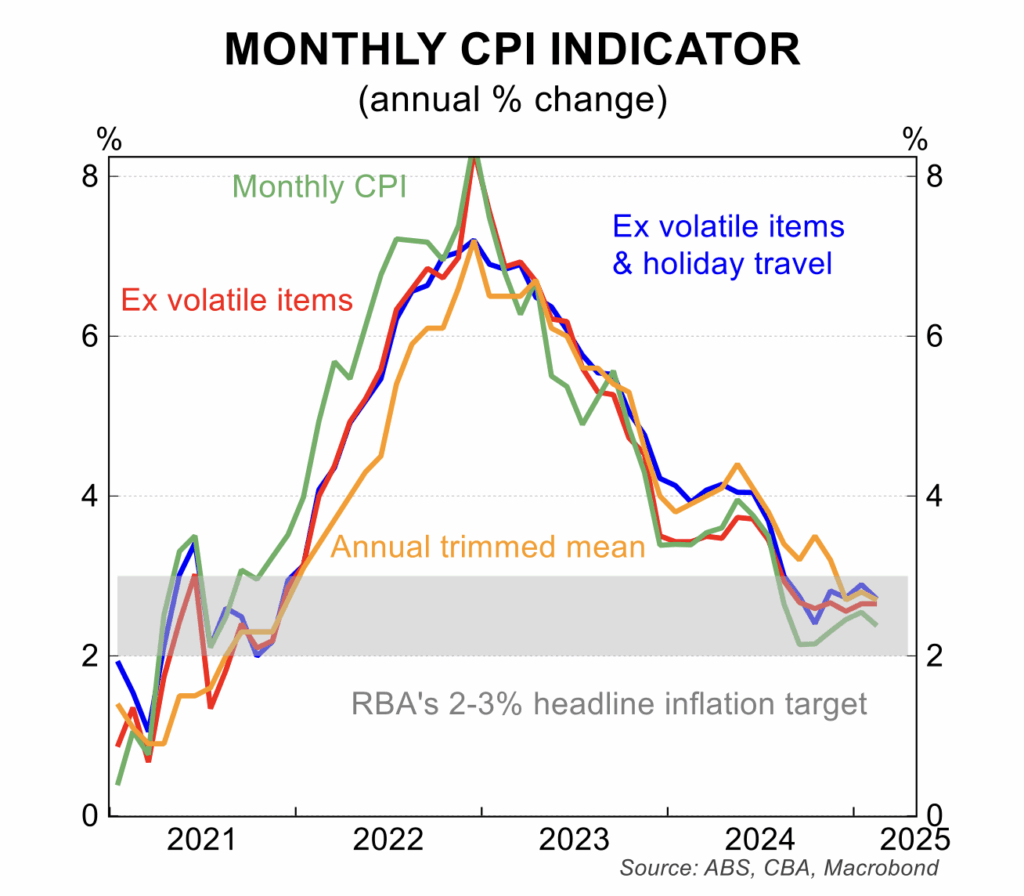

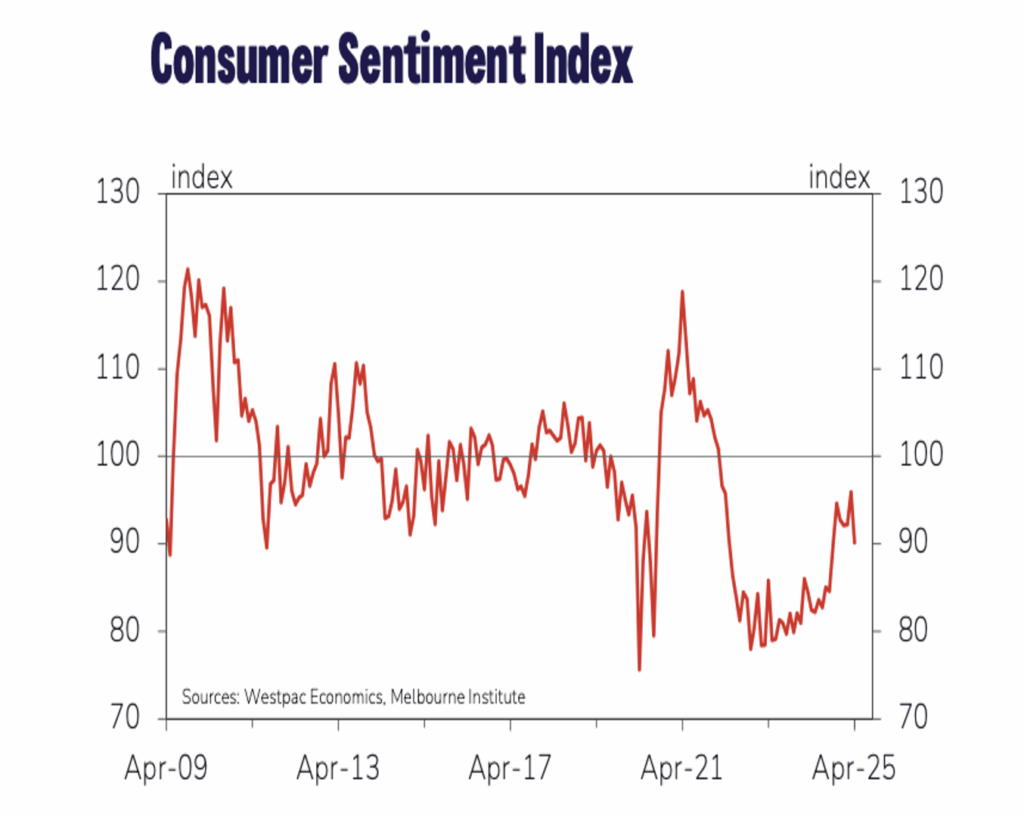

Significant downside risks to economic growth and higher inflation – that is the combination of news unfolding in the Australian economy over the past month.

The volatility in sentiment and

STOCKHEAD & THE AUSTRALIAN

As global volatility reshapes portfolios, private credit is drawing increased attention – but not all strategies carry the same risks, particularly when comparing US corporate

Stephen Koukoulas opens his April update by highlighting the dominant forces now shaping the economy and financial markets: oil prices, petrol supply, inflation, and interest rates.

These factors are