In our latest webinar, Zagga’s Economist-in-Residence, Stephen Koukoulas, examines the unpacks inflation, interest rates, housing divergence and the policy path ahead that are shaping Australia’s economic trajectory in 2026.

AUSBIZ

The growth of Australia’s real estate private credit market is gaining significant attention, with the segment forecast to near $90 billion by the decade’s end. In this Ausbiz

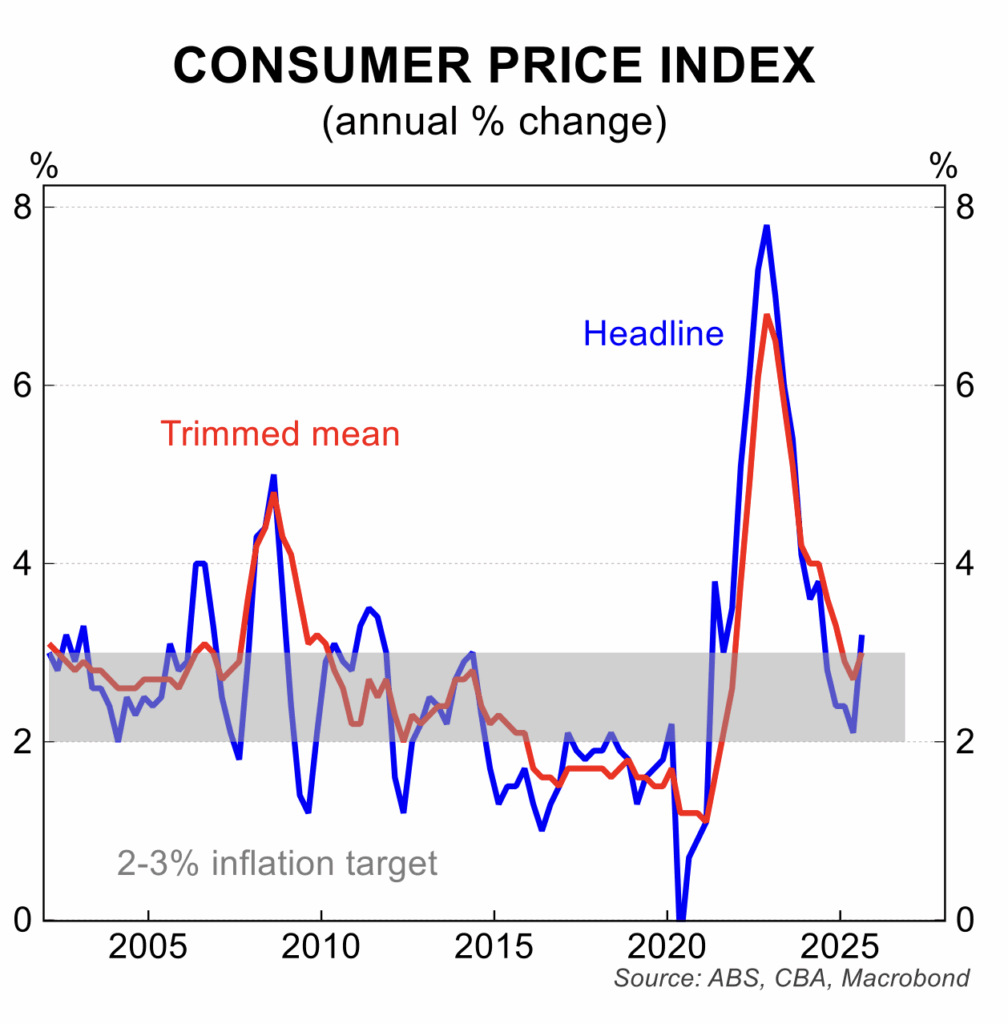

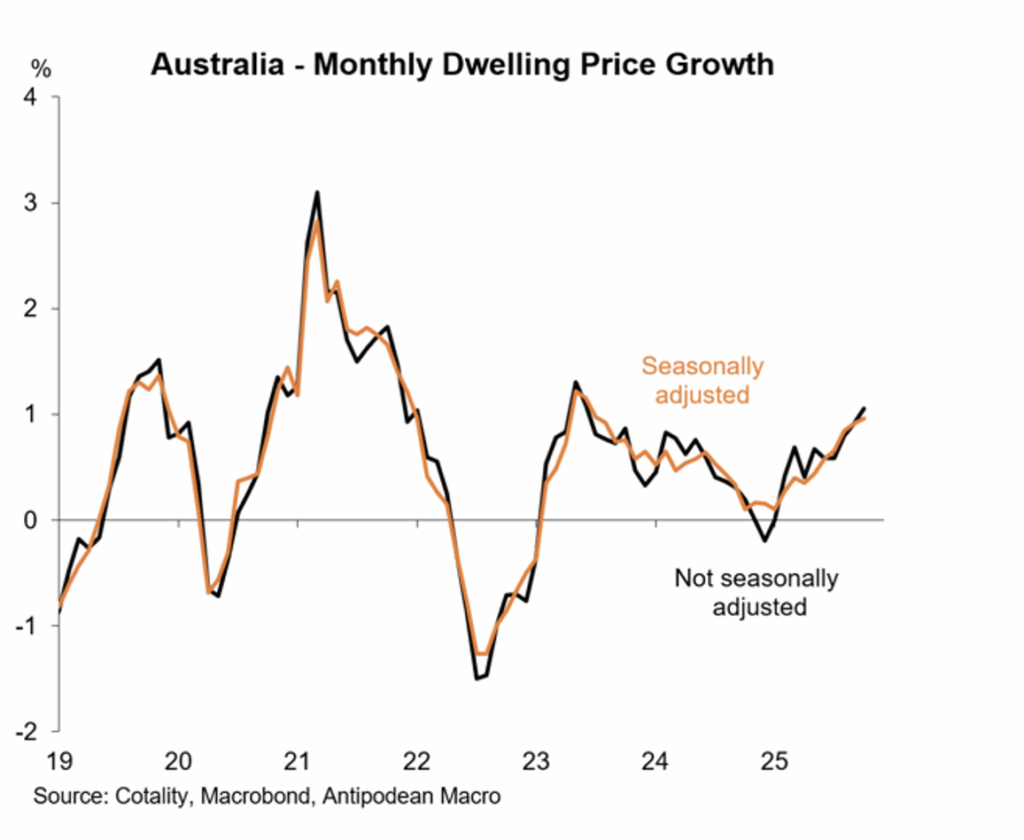

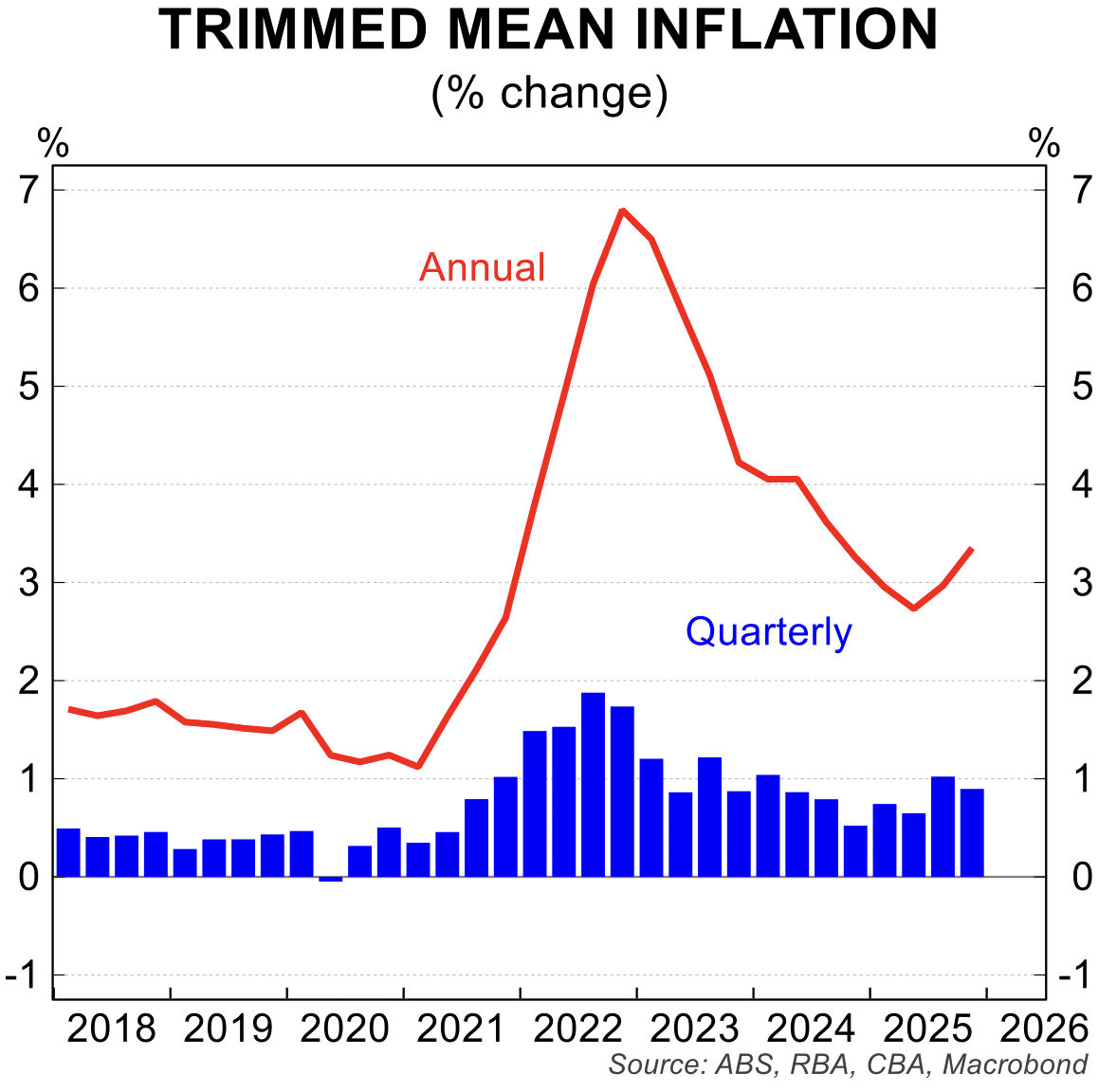

The sudden and unexpected about-face in economic conditions saw the RBA move from cutting interest rates with a bias for more cuts in August 2025, to hiking them with a