• Volatile markets are pushing investors toward predictable income

• $40B in hybrid capital may soon need a new home

• Housing shortages and tighter bank lending are boosting private credit

With market twists and turns, investors searching for reliable income are increasingly turning their attention to real estate private credit.

Markets have a habit of reminding investors who’s really in charge.

One minute everything looks calm. The next, oil prices lurch higher, inflation fears creep back into the room, and equity markets start throwing furniture.

When the world feels this turbulent, investors usually stop dreaming about moonshots and start thinking about defence.

The kind that helps preserve capital, generate income and avoid being whacked every time markets throw another tantrum.

Shares can be brilliant, yes, until they are not.

Bonds are meant to bring stability, but they still move around with interest rate expectations and broader market sentiment.

So, the search is on for something more reliable. Something that can generate steady income without asking investors to stomach daily market mood swings.

The hunt for steady income

Increasingly, one asset class finding its way into that conversation is real estate private credit.

According to Zagga CEO and co-founder Alan Greenstein, whose firm specialises in real estate private credit, the appeal is straightforward.

“In times of volatility, there is normally a flight to safety of some kind,” he told Stockhead.

“And safety in investment terms often means more predictable, more certain, more stable, less risky, less volatile asset classes.”

Private credit, he explained, sits squarely in that category because the return comes from contracted income rather than market price movements.

“You’re lending money to somebody, so you’re creating a debt. That debt is repaid, so you’re earning interest. You’re not relying on any capital growth.”

And in today’s market, where stock prices are swinging from one day to the next, that kind of steady income is becoming increasingly attractive.

Where private credit fits in a portfolio

For most investors, the traditional portfolio has long revolved around three pillars: shares, property and bonds.

Greenstein believes real estate private credit sits closer to the fixed income side of that mix, but with an important difference.

Traditional fixed income assets like bonds and hybrids are still traded in markets. That means their prices move around as interest rates change or investor sentiment shifts.

“If you plot the growth against bond or hybrid indices, you will see there is still volatility in those investments,” Greenstein said.

Private credit works differently.

Because the loans are privately negotiated and typically held to maturity, the income stream is largely predetermined.

“If I’m giving you a million dollars and you’re paying me 10% every month, it doesn’t matter what the markets are doing. I’m collecting my return every month,” he said.

For investors trying to reduce exposure to market swings, that steadier return profile can be appealing.

The hybrid exit and the SMSF opportunity

Another shift happening quietly in Australia could also push income-focused investors to look elsewhere.

Bank hybrid securities – long a favourite among retirees and income investors – are being gradually phased out by regulators, leaving around $40 billion of capital needing a new home over time.

Hybrids traditionally sat somewhere between bonds and shares, offering regular distributions while still trading on the stock exchange.

Greenstein believes their disappearance raises a natural question for investors seeking reliable income.

“The value of a hybrid to an investor was the coupon you collect on it,” he explained.

“So, if you had a hybrid paying 6.5%, you knew you would receive that distribution.”

That predictable income stream is exactly what many investors were buying hybrids for in the first place.

But as hybrids wind down, some investors are starting to look at similar alternatives.

“A natural place to go is to start looking at real estate private credit. You’re going to get the same kind of predictable distribution, but you’re not going to have the volatility.”

Greenstein acknowledges there is a trade-off.

Unlike hybrids or shares, private credit investments are not typically traded on a stock exchange, meaning investors give up some liquidity.

But in return, they may receive higher and more predictable income.

“While investors trade off liquidity, the payoff is the higher returns from private credit.”

That dynamic may be particularly relevant for self-managed super funds (SMSFs).

Historically, a large portion of SMSF money, roughly about 70%, has sat in bank deposits.

That behaviour suggests many SMSF investors favour simple, set-and-forget style investments that generate steady income without needing to trade in and out of markets.

In that sense, real estate private credit can behave in a way that feels familiar to those investors.

Zagga’s own data suggests that shift may already be underway, with SMSF allocations to its private credit strategies rising more than 24% year-on-year.

“When you invest in real estate private credit, it can also be set-and-forget. You’re getting paid monthly interest in a similar way that the bank pays you interest.”

“But you could be earning interest that is two or three times what you’re earning in the bank.”

“It’s important to remember, however, that private credit is higher up the risk curve than a bank-held term deposit so understanding the risk-return level you’re comfortable with is crucial,” he added.

The property advantage

Private credit covers many sectors, but in the real estate corner, there is one structural advantage: tangible collateral.

Unlike corporate credit or bonds, where repayment depends on a company’s balance sheet, real estate private credit is secured against a physical asset.

“I’d rather have the property at a decent valuation than the balance sheet.”

“It’s a much more defensive way of investing, particularly in turbulent times.”

That said, private credit is not risk free.

“Private credit investments are not for all people,” Greenstein admitted. “Every single investment carries a measure of risk.”

Greenstein stressed that it is best suited to sophisticated investors, those who understand the asset securing the loan, the loan purpose and timeframe, how much is being invested, and most importantly, who is managing the investment.

A growing market

The rise of private credit in Australia is also being driven by a structural shift in property finance.

Banks still fund the majority of the market, but regulatory changes have made construction lending more capital-intensive for them.

That has created space for private lenders to step in.

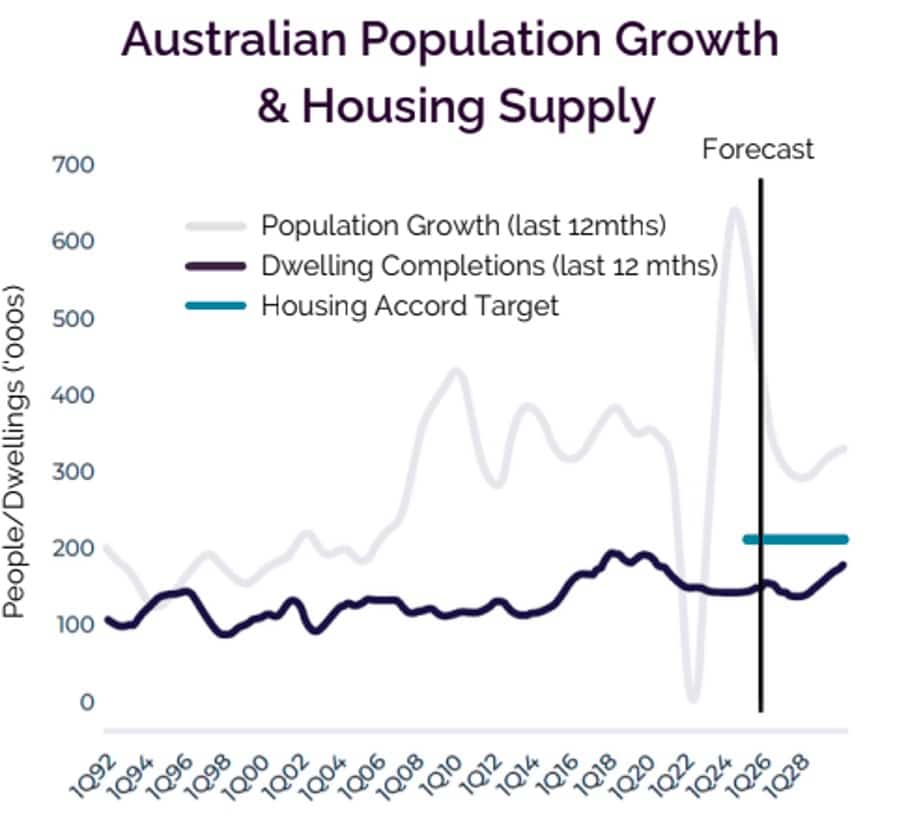

At the same time, Australia faces a massive housing shortage.

Greenstein said the numbers highlight the scale of the demand, with the Australian government predicting the population will grow by another 9 million people over the next 25 years.

“Those extra nine million people require another 3.8 million homes,” Greenstein said.

That demand is helping bring private credit further into the financial mainstream.

Greenstein says this opportunity is increasingly attracting global capital, with investors from the US and Asia viewing Australia’s private credit market as ripe for expansion.

And for investors searching for steady income in unpredictable markets, the sector is becoming harder to ignore.

This article was developed in collaboration with Zagga, a Stockhead advertiser at the time of publishing.

This article does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions.