STOCKHEAD & THE AUSTRALIAN

‘Turbulent’ is how many investors define the month that was.

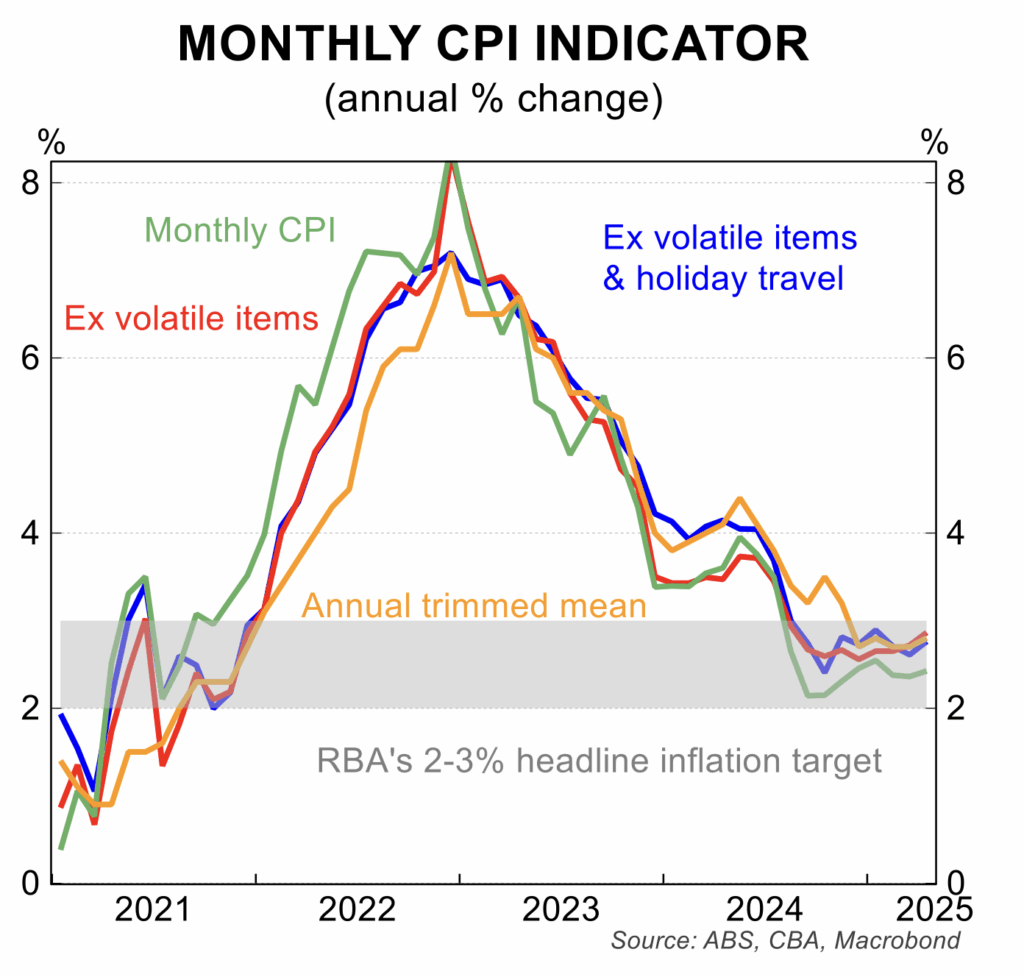

Locally, the Reserve Bank of Australia (RBA) passed on a rate rise due to stubborn

INVESTOR DAILY

Private credit is no longer a niche allocation, it is a core component of sophisticated portfolios – and nowhere is this more evident than in Australia’s real

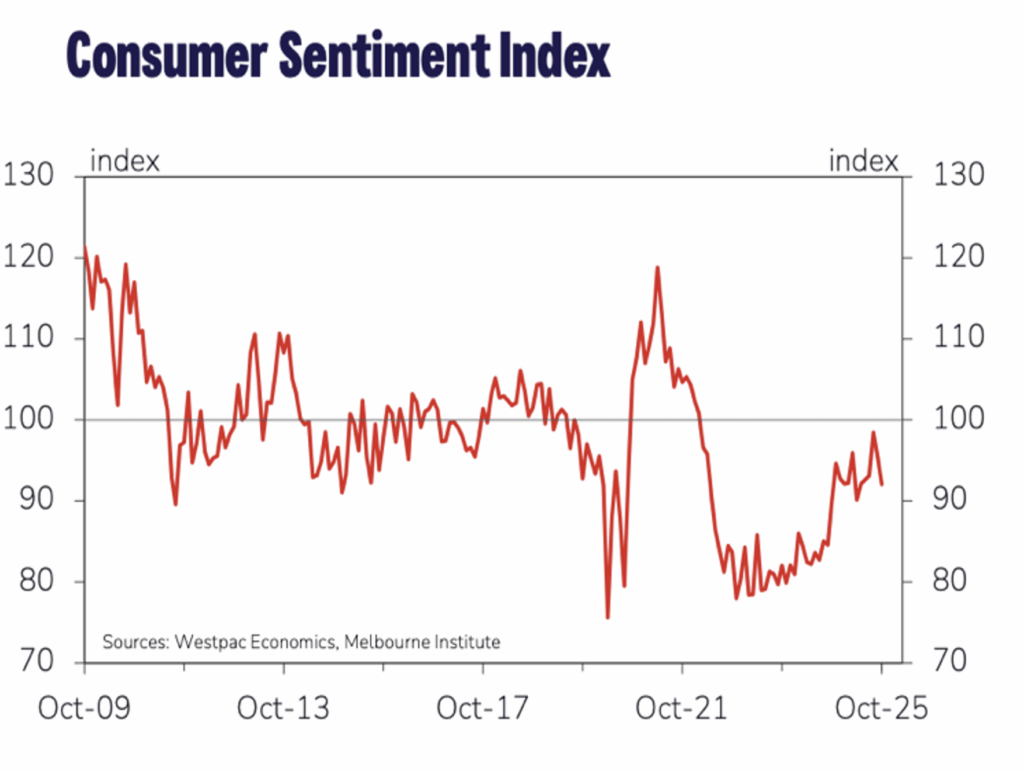

The earlier cautious optimism about an economic recovery is translating to confirmation about broader economic strength. While serious uncertainties dominate the global outlook amid elevated geopolitical threats to markets and