Summary: 'Two Minutes for Zagga' | July 2025

The Reserve Bank of Australia surprised markets and economists alike this month by holding interest rates steady, despite clear signs that inflation is returning to target levels. The decision, announced on 8 July, came as a surprise to many who had expected a rate cut, given the recent softening in inflation data.

Why the RBA held rates

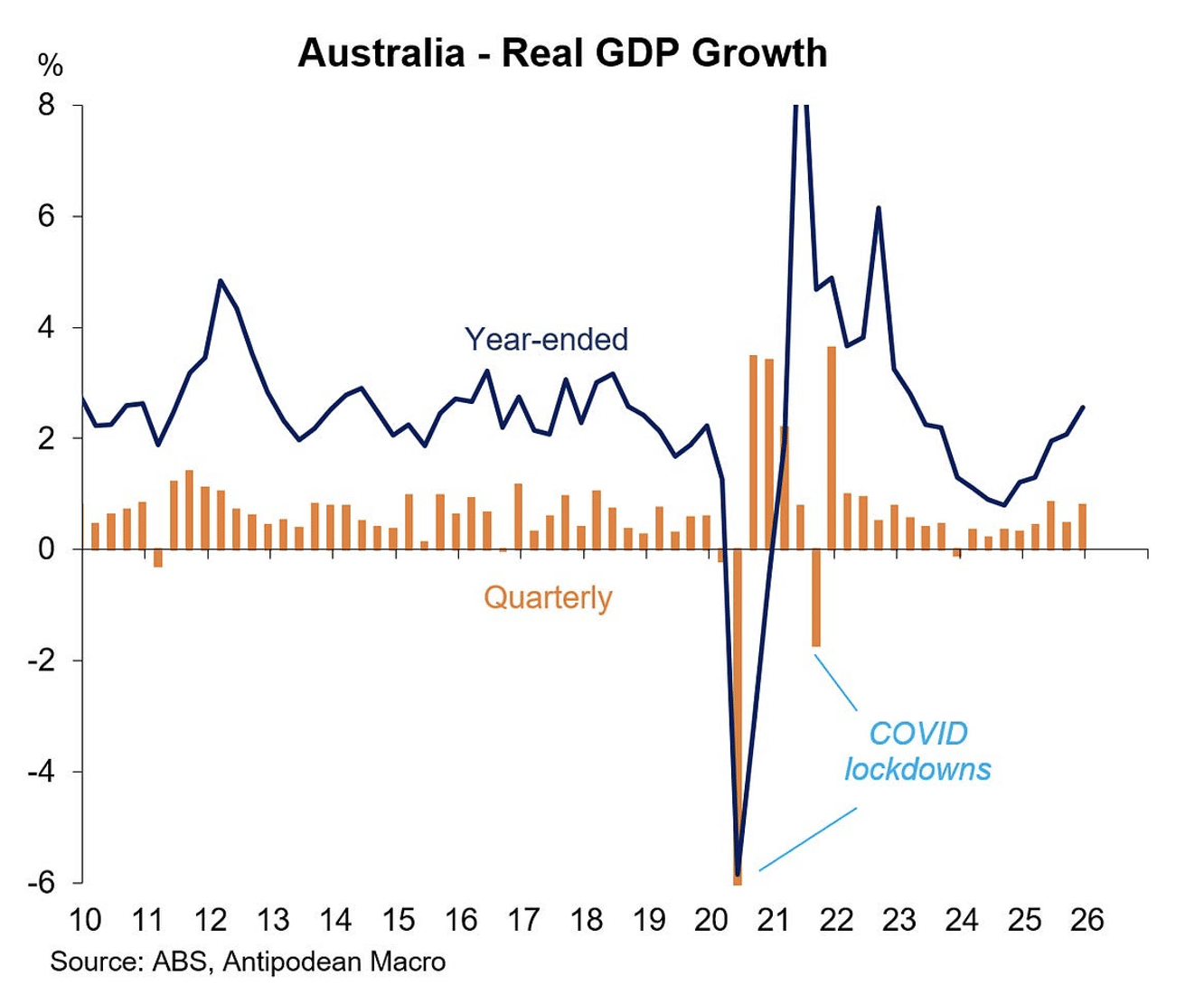

The RBA’s reasoning comes down to caution. While headline inflation dropped to 2.1% in the year to May, and the trimmed mean (their preferred underlying measure) eased to 2.4%, the central bank remains concerned about potential inflationary rebounds – particularly into 2026. They’re also watching the labour market closely. With unemployment sitting at just 4.1% and productivity growth still weak, the RBA signalled that conditions aren’t yet ideal for sustainably meeting its 2–3% inflation target.

In short, the direction of rates hasn’t changed – but the timing has. The market still anticipates rate cuts later in the year, just not as soon as originally expected.

The state of the economy

- Consumer spending and retail sales have shown modest improvement following earlier rate cuts in February and May. However, momentum could stall if rate relief is delayed further.

- Building approvals, which showed strong growth earlier in the year, have now declined for two consecutive months – a concerning trend in a housing market already facing supply shortages.

- House prices continue to edge upward, particularly in previously softer markets like Sydney and Melbourne. Meanwhile, growth remains strong (though slowing) in Brisbane, Perth, and Adelaide.

Global factors still looming

International developments are adding another layer of uncertainty. From tariff tensions – including delays in new U.S. measures – to ongoing geopolitical risks in regions like the Middle East, Ukraine, and Taiwan, global instability remains a key watchpoint for investors and policymakers alike.

What to expect next

For now, the RBA’s message is clear: they’re not ruling out rate cuts, but they need more confidence before moving again. Upcoming inflation and labour market data will be pivotal in shaping the timing of any future decisions.

In the meantime, the broader economy continues to walk a fine line between resilience and stagnation. For investors and private credit markets, this creates a landscape where caution and opportunity go hand in hand.

Watch the full video below.

Stephen Koukoulas is Managing Director of Market Economics, having had 30 years as an economist in government, banking, financial markets and policy formulation. Stephen was Senior Economic Advisor to Prime Minister, Julia Gillard, worked in the Commonwealth Treasury and was the global head of economic research and strategy for TD Securities in London.